Executive Summary

- Our base case scenario is that most major developed economies will avoid recession in 2025, but policies are in flux and the outlook is especially uncertain.

- We think the US economy is likely to see the sharpest slowdown among major developed economies in 2025, with growth slowing to between 0%-0.5%, with potentially a quarter or two of negative growth (technical recession) depending to what degree announced tariffs are (or are not) moderated and the degree to which the Fed and Treasury are willing to intervene to stabilise markets as needed. Strong aggregate household, company and bank balance sheets coming into this period reduce the risk of a deep 2008/09 type of financial crisis-led downturn in our view.

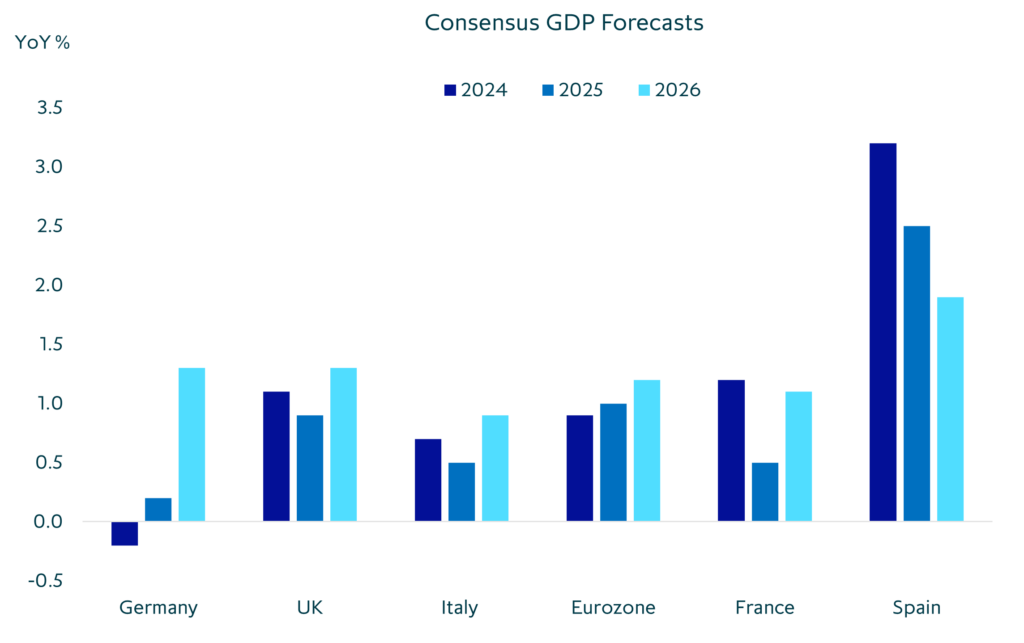

- In our view, most European economies will continue to see positive growth in the 0.5%-2% range in 2025, with increased fiscal stimulus and ECB rate cuts helping to offset tariff disruption. Although the UK is likely to see a relatively small negative impact from US tariffs, fiscal constraints and sticky inflation give policymakers less leeway to support growth than in Europe. Therefore, while we think UK growth in 2025 will remain positive, GDP growth in the 0.5%-1% range seems more likely.

- Europe, the UK and other countries are likely to benefit from lower goods prices as China and other affected exporters divert goods formerly destined for the US market. Lower relative input costs should boost competitiveness relative to US companies contending with higher input costs and disrupted supply chains. Europe will additionally benefit as the dramatic realignment of US economic and geopolitical priorities accelerates Europe’s move towards more cohesive and coordinated regional economic, financial and defence policies.

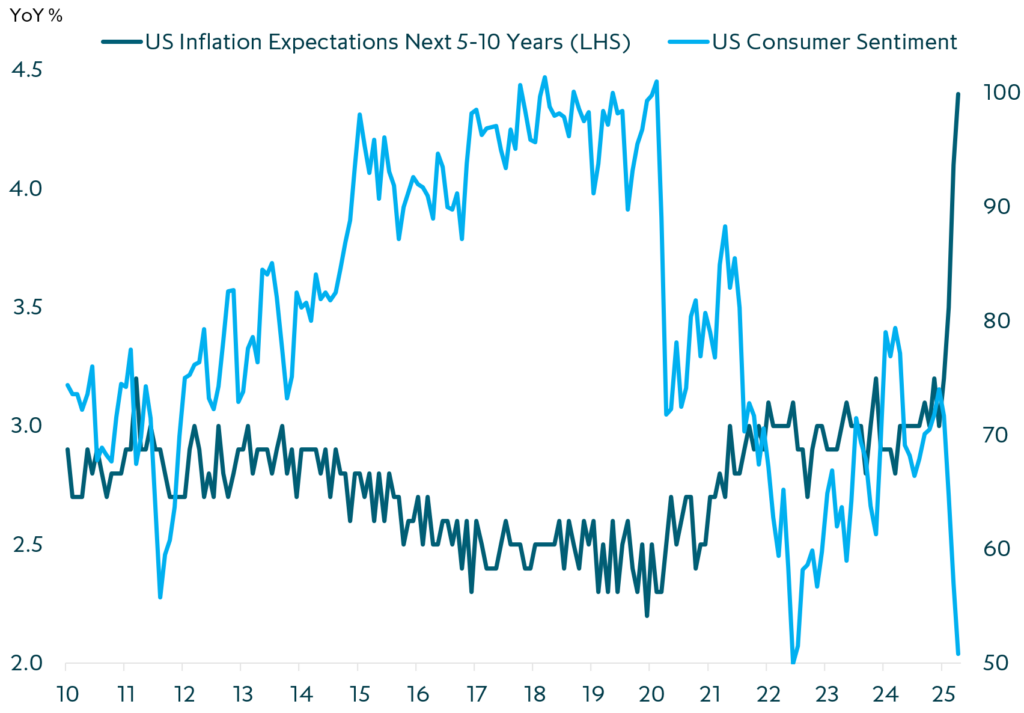

- While the ECB has scope to cut rates another 50-100bp this year, the Fed and BoE are constrained by sticky core inflation and – particularly in the US – heightened inflation expectations. Until inflation expectations are clearly under control, an extended rate cutting cycle seems unlikely. The BoE is facing a similar situation, but most lead indicators point to more rapid core inflation declines in the coming months, which should allow the BoE to push through more aggressive rate cuts in the coming months.

- The tariff war will likely dampen Asia-Pacific growth but not substantially damage it. Lower energy prices and lower import prices from China should push inflation down and provide central banks room to ease monetary policy to support growth if needed. China will likely offset a large part of the US tariff hike impact through easier fiscal and monetary policy and a weaker yuan.

- The business operating environment will likely become more difficult for a number of companies across all markets, but performance dispersion is likely to be high. While some companies in manufacturing/industrial sub-sectors will be hit by the higher US tariffs (e.g. autos and auto related companies), we (and most of the private markets industry) tend to have limited exposure to these areas – with the bulk of our investments in less cyclical services related businesses that are well-insulated from the direct effects of the trade war.

- It is too early to fully assess the secondary effects of a potential slowdown in the US economy, potential sustained lower asset prices and higher policy uncertainty. We will be monitoring sentiment and purchasing manager indicators and company fundamentals in the coming months to gauge the potential magnitude of these secondary effects and their impact on the broader global economic outlook and business operating environment.

Jump to:

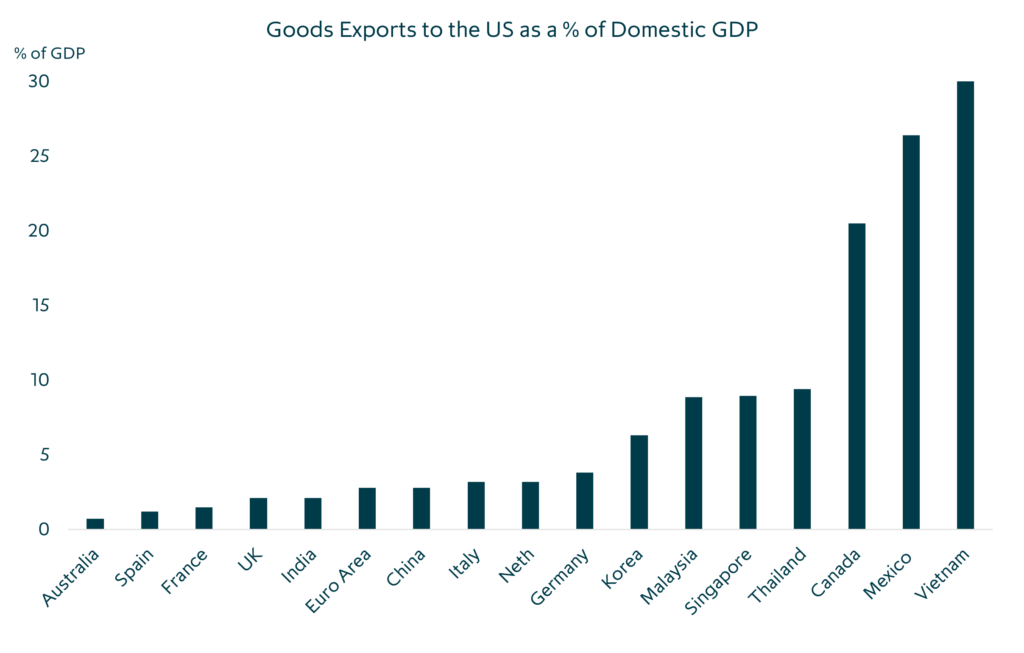

Country exposure to US import tariffs varies widely

US Views

US President Donald Trump’s announced tariffs mark the biggest upheaval to international trade policy since US President Herbert Hoover signed the Smoot-Hawley Tariff Act in 1930. The Budget Lab at Yale (TBL) estimates that on tariff polices announced through 7 April 2025, the US average effective tariff rate will be 22.5%, the highest rate since 1909. On their calculations this will push US inflation up by 2.3% in the short-run, reduce US GDP growth by 0.9 percentage points in 2025, and reduce the size of the US economy by 0.6% persistently.

In the US, companies that are likely most at risk from weaker consumer sentiment and spending power are those in discretionary categories such as apparel, furniture and consumer electronics.

It is estimated that the tariffs announced so far, if fully implemented, will most strongly affect clothing and textiles prices, with TBL estimating apparel prices will rise 33% and food prices 4.5%, around three times recent grocery inflation. These price increases will disproportionally hit middle-to-lower income households given the larger share of budgets spent on basic necessities, reducing discretionary spending power. Companies that are likely most at risk from weaker consumer sentiment and spending power are those in discretionary categories such as apparel, furniture and consumer electronics. Companies in the auto and related sectors are also likely to be affected by supply chain disruptions, higher input prices, squeezed margins and likely lower sales volumes on reduced consumer purchasing power.

US tariffs do not cover services, so the direct impact on services businesses is expected to be minimal. However, the impact of heightened policy uncertainty on broader economic activity will need to watched carefully, with business and consumer sentiment surveys key indicators to monitor. Recent US consumer and business sentiment indicators have dropped sharply. If the recent turmoil in financial markets is not reversed the effective tightening of financial conditions will likely further weigh on business investment and household consumption, with ramifications across all sectors.

We are focused on identifying those companies and industries which will continue to grow despite potential broader economic headwinds.

That being said, we believe a number of sectors should remain relatively insulated from the disruptions, including parts of the healthcare, financial services, and business services sectors, as well as certain segments of the technology sector. While economic growth may be diminished in the near-term, the US will continue to produce and grow some of the world’s market leading companies. We are focused on identifying those companies and industries which will continue to grow despite potential broader economic headwinds.

Rising stagflation risks in the US

Europe and UK Views

Only around 3% of EU GDP and 2% of UK GDP is directly exposed to the US goods market, limiting the overall direct economic impact of the hike in US tariffs on goods. Around 85% of the EU and UK economies are services-related and this segment of the economy will not be directly affected by the new US tariffs.

The recent watershed changes in German and EU-wide fiscal policy to allow a significant rise in infrastructure and defence spending, marks a once-in-a-generation shift in fiscal policy.

Therefore, the overall medium to long-term impact on European and UK. growth is expected to be relatively small. Using ECB calculations, the impact of a 20% tariff on all EU goods exported to the US would reduce EU growth by around 0.24 percentage points if there is no retaliation by the EU, and up to a maximum of 0.40 percentage points with full retaliation (we believe any retaliation will likely be limited and focused), with the brunt of the impact concentrated in the first year after the rise in tariffs, and then diminishing with time. Private sector estimates of the impact of US tariffs on the EU economy are generally lower than the ECB estimates above.

The impact on the UK economy of the announced 10% tariff on UK exports to the US (and taking account of the global 25% tariff on autos & parts, steel and aluminium exports to the US) vary widely, but they are generally estimated to be around half or less than half the size of the impact on the EU economy – not surprising given the UK’s lower export exposure to the US and lower tariff rate.

The impact on the UK economy of tariffs on UK exports to the US vary widely, but they are generally estimated to be around half or less than half the size of the impact on the EU economy.

The recent watershed changes in German and EU-wide fiscal policy to allow a significant rise in infrastructure and defence spending, marks a once-in-a-generation shift in fiscal policy. This should provide a medium to long-term boost to Europe’s growth rate – and at the very least provide downside growth protection. This shift in policy may help offset any secondary effects from the ongoing global tariff turmoil.

While specific companies in manufacturing/industrial sub-sectors will likely be hit by the higher US tariffs (e.g. autos and auto related companies), we (and most of the private markets industry) tend to have very limited exposure to these areas – with the bulk of our investments in less cyclical services related businesses that are well-insulated from the direct effects of the trade war.

It is too early to fully assess secondary effects of a potential slowdown in the US economy, sustained lower asset prices and higher policy uncertainty. We will be monitoring sentiment and purchasing manager indicators in the coming months to gauge the potential magnitude of these secondary effects and their impact on the broader economic outlook.

Like most of the private markets industry, we have limited exposure to affected manufacturing and industrial sub-sectors – with the bulk of our investments in less cyclical services-related businesses that are well-insulated from the direct effects of the trade war.

Europe growth expected to remain resilient

Asia-Pacific Views

The outlook for Asia-Pacific economies varies widely by country, with smaller more open economies likely seeing a larger hit from the current trade war than those with larger and more insulated domestic markets.

China will take a relatively big hit given the magnitude of the tariff increases it is faced with but easier fiscal and monetary policy and likely further yuan weakening should help ease the blow.

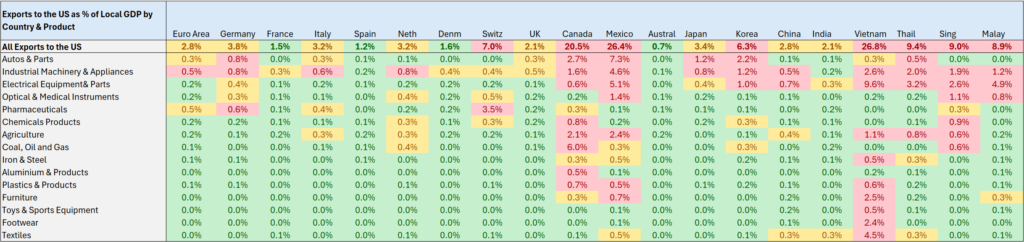

Of the major Asia-Pacific countries, Australia, India, China and Japan have the lowest goods export exposure to the US market relative to GDP (3% and below) with Vietnam an outlier in its very large economic exposure to the US goods market (27% of GDP). Thailand, Singapore, Malaysia and Korea lie somewhere in the middle with US export to GDP ratios in the 6%-9% of GDP range. China will take a relatively big hit given the magnitude of the tariff increases it is faced with (and is hitting back with), but easier fiscal and monetary policy and likely further yuan weakening will likely help ease the blow.

Perhaps more important than country level exposures are the varied range of sector exposures. Even if the recently announced (and now postponed) “reciprocal” tariffs are not fully implemented, there will likely be large differentials in performance at a sector level. Some of the most exposed sectors include autos and parts, electrical and machinery equipment, agricultural products, textiles and clothing.

Services business are not being directly targeted by the Trump administration’s new trade tariff regime and most services businesses should remain relatively unscathed. However, secondary effects from potentially slower domestic and global growth, and exposures to businesses directly tied to international goods trade will need to be monitored.

In Asia, some of the most exposed sectors include autos and parts, electrical and machinery equipment, agricultural products, textiles and clothing, with most services businesses relatively well-insulated.

On our base case that US growth slows but deep recession is avoided, and that Europe and UK growth is sluggish but positive, the global economic environment should remain supportive for most Asia economies. It is likely that China goods exports to non-US countries will ramp up and prices will come down as many Chinese companies are forced to divert product away from the US market. While this may have a negative impact on domestic competitors, it will also likely help push goods inflation down and allow central banks to cut interest rates more swiftly if domestic growth concerns warrant it.

On balance, we think the ongoing tariff war will dampen Asia-Pacific growth but not substantially damage it. Lower energy prices and lower import prices from China should push inflation down and provide central banks room to ease monetary policy (and allow currencies to weaken) to support growth if needed. The biggest likely impact of the tariff war is likely to be at a sector level, with autos and parts, electrical and machinery equipment, agricultural products, textiles and clothing most at risk and most services businesses relatively well-insulated.

Country and Sector Exposures to the US Goods Markets

Source: Bloomberg, April 2025. Calculations based on data for calendar year 2023. Legend: Green 0%-0.24%, Amber 0.25%-0.49%, Red 0.50%+ of GDP.

Go deeper

- Listen or watch Nick Brooks’ 14 April appearance on Bloomberg’s Daybreak Europe and The Opening Trade (17mins into the show)

- Read Nick’s latest US and European Private Company Trends analysis (ICG Clients Only) or a short summary

- Watch video case studies across our portfolio (ICG Clients Only)