Executive summary

Bucking the trend

Private companies in Europe, the UK and the US performed strongly through the first nine months of 2024, according to data tracked by the proprietary ICG Private Company Database. The database tracks key financial metrics of around 500 US and European private companies on a quarterly basis, providing unique insights into the structural fundamentals of companies that make up the private markets universe.

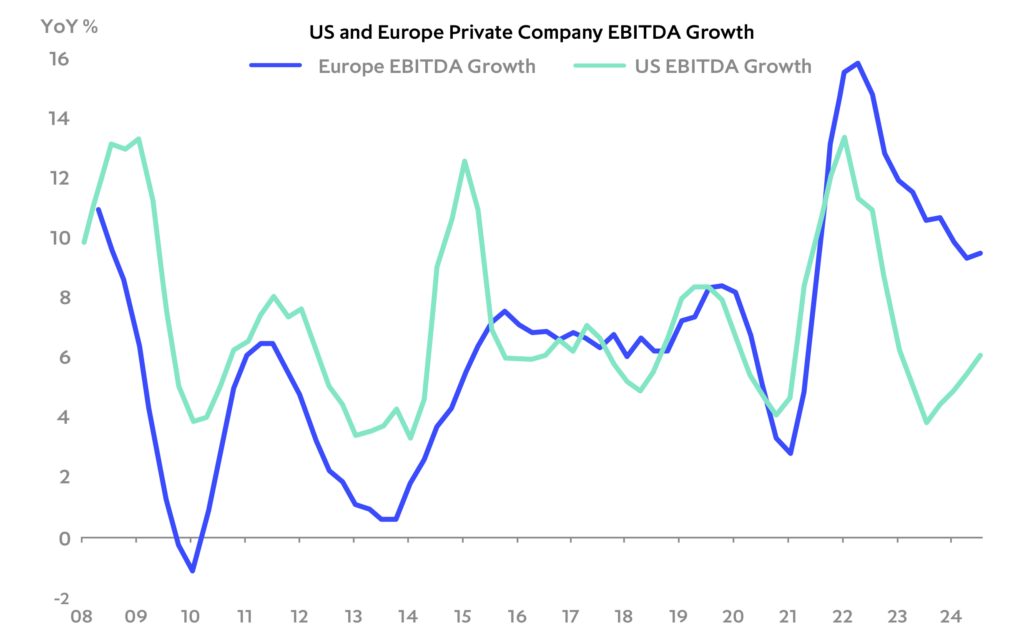

Europe and UK private companies continued to outperform their US counterparts, bucking the trend of relatively weak headline GDP growth. The EBITDA growth outperformance reflects a combination of a more favourable sector and company mix and more resilient margins. Median EBITDA growth for Europe and UK domiciled private companies rose by an average of 9.6% in the first nine months of the year, with momentum picking up in the third quarter.

Sustained strong performance of Europe and UK EBITDA growth despite weaker headline GDP growth may seem counter-intuitive at first. However, as detailed in this report, private companies tracked by ICG’s Private Company Database have limited exposure to the heavy industry and manufacturing sub-sectors that have been the main cause of the weakness in Europe’s headline GDP numbers. Private company exposures tend to be in areas where European and UK companies have generally thrived, with higher relative weights in fast-growing sectors such as software and services, commercial and professional services as well as consumer staples. Median margins in overweighted sectors have also tended to hold firm.

US private companies also performed well in the first nine months of 2024. US EBITDA growth has been on an accelerating trend since bottoming in Q3 2023, with improving margins – particularly in the consumer discretionary and healthcare sectors – supporting growth. US private company median EBITDA growth rose by 5.5% in the first nine months of the year and accelerated to 6.1% in the third quarter, with company-level guidance pointing to continued healthy growth in 2025.

Debt sustainability measures have held up well, with strong EBITDA growth helping to offset continued high interest rates. In Europe, median leverage (Net Debt/EBITDA) stood at 4.8x in Q3 2024 and the median interest coverage ratio (EBITDA/Cash Interest) appears to have stabilised at a comfortable 2.6x. In the US in Q3 2024, the median leverage ratio stood at 5.4x and the interest coverage ratio held steady at 1.9x. With interest rates at or near peak and underlying growth still strong, it is likely that debt metrics will continue to stabilise in 2025.

Despite substantial geopolitical uncertainty and potential policy risks, private companies tracked by ICG’s Private Company Database appear to be well-positioned for the year ahead. A focus on less-cyclical services-related sectors, strong cashflow generation, balance sheet strength and pricing power has helped support private company performance through the major dislocations caused by the Covid pandemic and Russia’s invasion of Ukraine. We think these characteristics will hold private companies in good stead as we head into an uncertain 2025.

Resilient private company EBITDA growth