Key points

- Trump’s election win marks a watershed moment for the global economy and geopolitical landscape. Donald Trump’s US presidential win together with a Republican sweep of the US Congress puts Trump in a strong position to swiftly start implementing his economic and political agenda in early 2025. As his campaign proposals were very broad-brush, it’s too early to assess how his policies will play out. However, he has made clear that trade tariffs, immigration controls, regulatory easing and tax cuts are priorities.

- Trade tariffs expected to dampen growth, push inflation higher (initially). It remains to be seen how aggressively the Trump administration implements its planned tariff increases on goods. Statements by Trump during his campaign indicate potentially a 60% tariff on all China goods imports and 10% to 20% tariffs on all other countries goods imports. More recently he announced he would put a 25% tariff on goods imports from Mexico and Canada and add 10% to tariffs on goods imports from China. Most analyses indicate that a large rise in US tariffs would likely have initially an inflationary impact in the US, followed by a negative growth impact on all countries involved, with inflation falling as demand slows and base effects kick in. China would be particularly badly affected given the scale of the proposed China tariffs and the importance of the manufacturing sector to its economy. Offsets will likely include a weaker yuan and further fiscal and monetary stimulus measures.

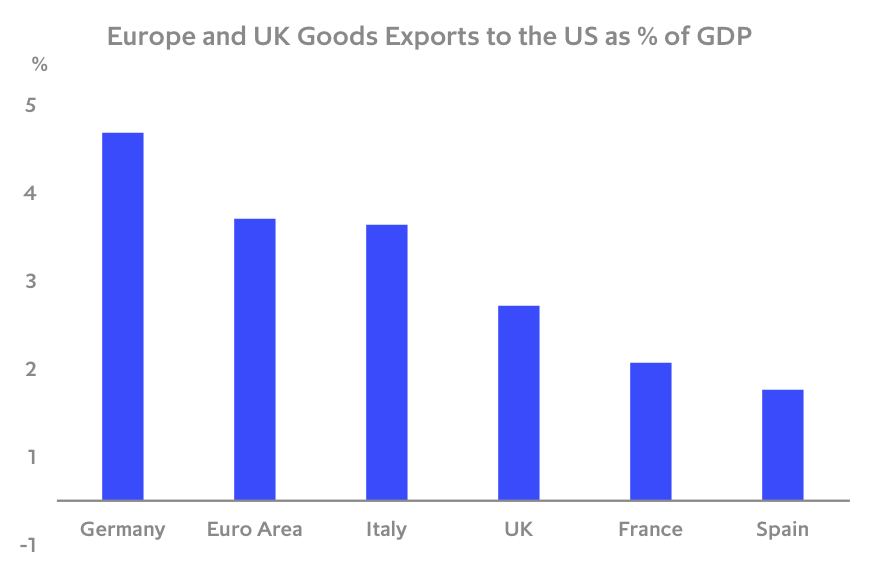

- US tariff rise impact on Europe and UK expected to be manageable. To put things in perspective, goods exports from Europe and the UK to the US in 2023 were equivalent to around 3.2% and 2.2% of GDP respectively. The services sector in Europe and the UK makes up around 80% of their respective GDPs, and most of the services sector should see little direct impact from higher US goods tariffs. While higher tariffs on goods has the potential to hurt parts of their manufacturing sectors – autos, pharmaceuticals and machinery in particular – the impact on the broader Europe and UK economies should be manageable in our view. The inflation impact is expected to be negligible given weakening underlying inflation pressures and likely only token, highly targeted retaliatory tariffs.

US government debt on an unsustainable trajectory

- Proposed US tax and regulatory policies are growth positive, but bring inflation and debt sustainability risks. An extension of the 2017 corporate tax cuts, reinstatement of expired investment incentives, promised new tax cuts on tips, overtime pay, a repeal of taxes on social security benefits, restoring of the state and local tax deduction and an easing of energy and financial regulations, if implemented, would be growth positive. However, with the economy already growing at full potential, further stimulus risks driving inflation higher. Higher inflation and government bond yields have the potential to derail growth if the Treasury doesn’t appear to have a credible plan to fund the proposed tax cuts.

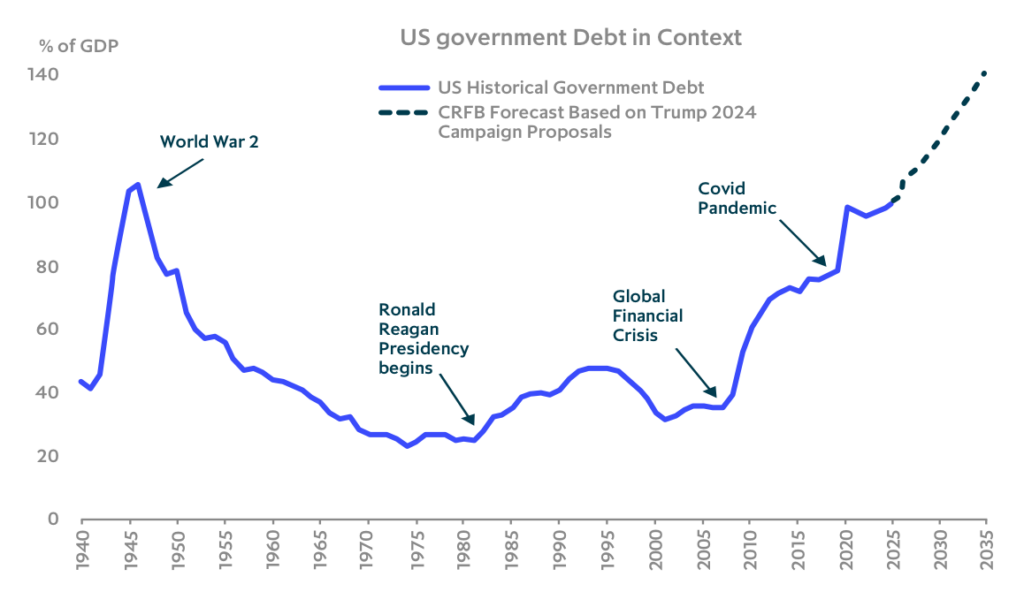

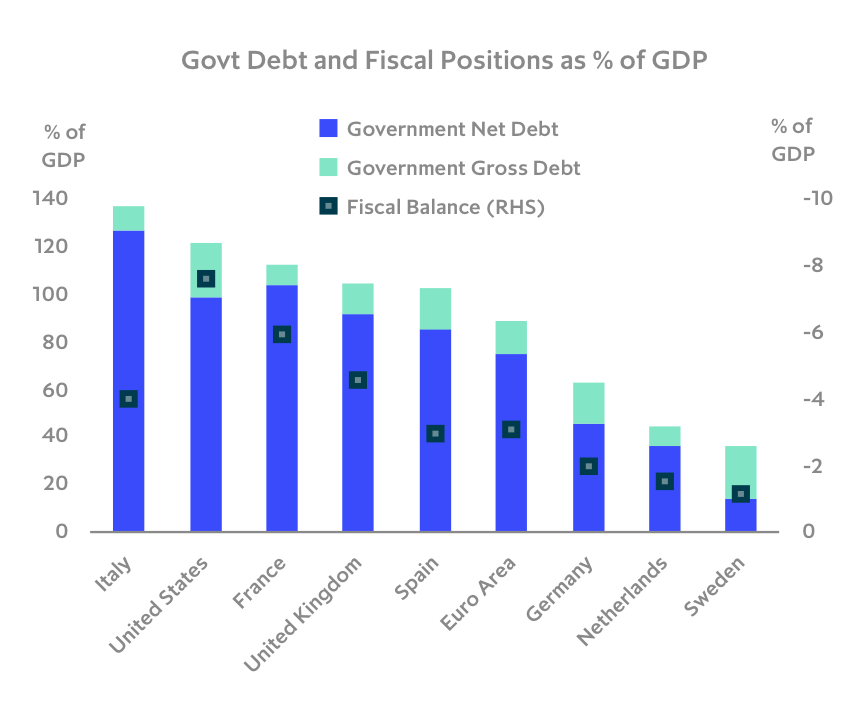

- Markets have given the administration-in-waiting the benefit of the doubt, but this could change. The market reaction to Trump’s win implies most investors assume many of Trump’s tax cut promises during his campaign will not be fulfilled and fiscal prudence will prevail. Our base case is key economic officials in the Trump administration recognise the risks of a potential bond market revolt and will therefore be careful to present credible fiscal plans. But Trump is unpredictable and has huge sway over his Cabinet and Congress. With the US fiscal deficit estimated at 7.6% of GDP this year and general government debt 122% of GDP, there is little room for error.

Executive summary

Donald Trump’s US presidential election win and the Republican sweep of the US Congress is a watershed moment for the global economy and geopolitical landscape. It is too early to make any definitive statements on how his administration will affect global markets and economies, but a few key themes stand out.

The first is that Trump has made clear he intends to raise tariffs on imported goods, with China likely facing the brunt of the increases. The second is that he plans to cut US taxes and regulations, though it is not yet clear how deep the cuts will be and how the tax cuts will be paid for. And third, on the geopolitical front, his early administration appointments indicate he will likely pursue an “America First” isolationist-leaning, transactional foreign policy, similar to his first term.

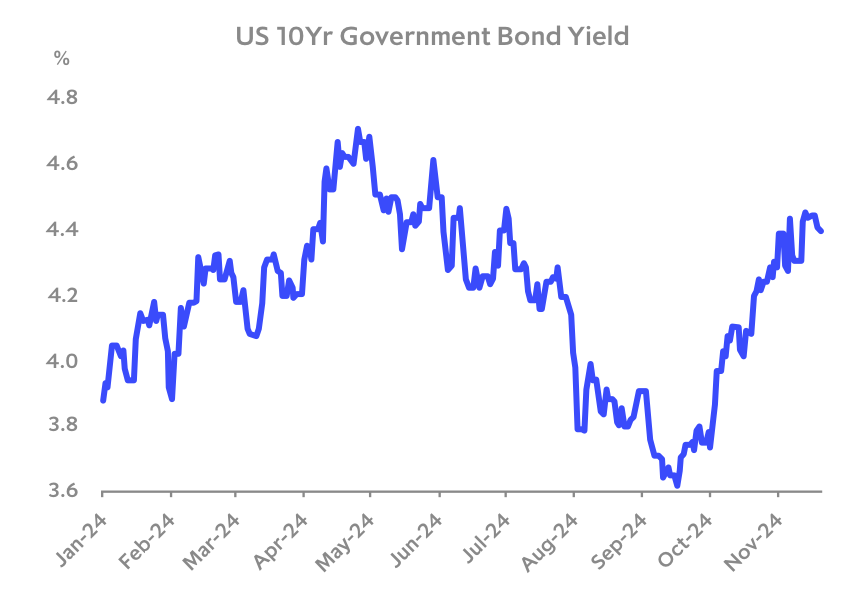

The initial market reaction to his win has been relatively orderly, with US risk assets and the US dollar out-performing, and government bond yields stabilising following a large pre-election rise. Looking forward, a key risk to the outlook is a potential back-up in US government bond yields (with ripple effects through global markets) if the new Trump administration tries to push through tax cuts without a credible plan to pay for them.

Another key risk is an escalatory tit-for-tat global trade war that disrupts supply chains and drives global growth lower and (initially) drives inflation higher. Our base case is that cooler minds will prevail, and worst-case scenarios will be avoided, allowing the current global economic expansion to extend through 2025. However, Trump is notoriously unpredictable and without the constraints of divided government, his policies and the global outlook have the potential to change quickly.

US bond yields up, but an orderly rise – so far

The services sector makes up over 80% of Europe’s GDP, with most services companies seeing limited impact from higher US goods tariffs.

Assessing potential impact of Trump’s trade policy

While it is too early to make any firm judgements on how a Trump presidency will affect the global economy, there are a few clear areas where there will likely be major policy changes.

The first is trade policy. A key Trump campaign message is that his administration plans to raise tariffs on imported goods. Although very few specifics have been provided, during his campaign Trump indicated he wanted to put 60% across-the-board tariffs on goods imports from China and 10% or 20% tariffs on goods imports from all other countries. More recently he announced he would put a 25% tariff on goods imports from Mexico and Canada and add 10% to tariffs on goods imports from China. It remains to be seen how these policies might be implemented in practice. Last time tariffs were implemented on a less-damaging product- by-product basis to reduce the impact on US consumers.

What do higher tariffs mean for the US economy?

Most analyses indicate that a large rise in US tariffs will have a dampening impact on US domestic demand as real purchasing power is hurt by higher goods prices, and investment is hit by higher trade uncertainty, with some offset from government tariff revenues depending on the degree to which they are recycled into the economy through tax cuts and higher spending. On most analyses, higher import tariffs are initially inflationary as tariff costs are passed on to the consumer. However, ultimately slower demand growth as real incomes are hit, and base effects after the initial one-off price increases, causes inflation to come back down (with prices at a permanently higher level).

Europe and UK goods exports to the US as % of GDP

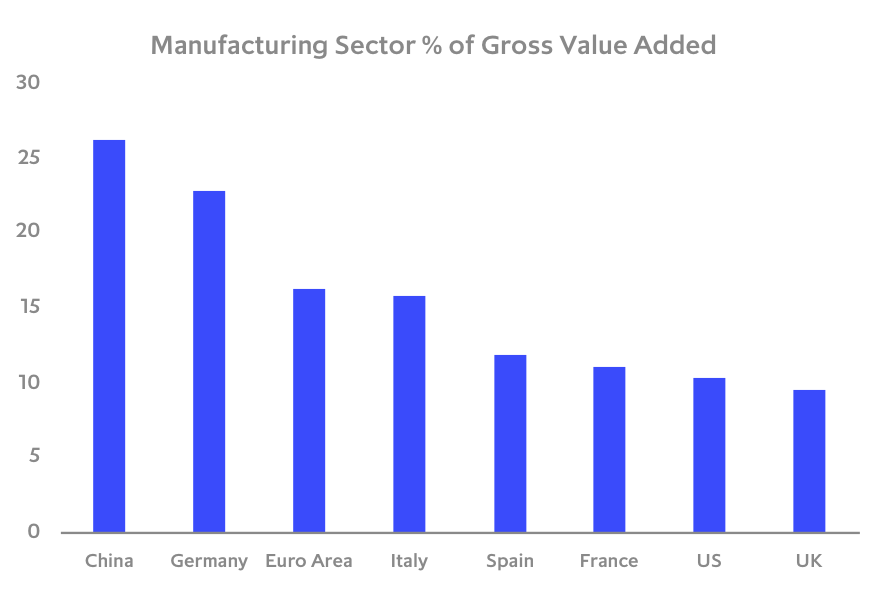

Manufacturing makes up small share of most developed economies’ GDP

The impact of higher tariffs on Europe is manageable

In terms of the potential direct growth impact on Europe, to put things in perspective, Europe’s goods exports to the US in 2023 were equivalent to around 3.2% of GDP. Even for Germany, the most exposed of Europe’s economies, goods exports to the US were equivalent to 4.2% of GDP. UK goods exports to the US are equivalent to 2.2% of GDP. The manufacturing sector makes up around 15% and the services sector makes up over 80% of Europe’s GDP. While services companies servicing domestic goods exporters exposed to the US may be affected, most services sector companies should see little direct impact from higher US goods tariffs.

Therefore, if Trump follows through on his threat to raise import tariffs on goods, while they will have potentially large consequences for parts of Europe’s manufacturing sector – autos, pharmaceuticals and machinery in particular – and may have secondary effects on companies servicing them, the impact on the broader Europe and UK economies should be manageable in our view. The inflation impact is expected to be negligible given already weak underlying inflation pressures and likely only token highly targeted retaliatory tariffs.

China likely to be most negatively affected by Trump policies

The potential impact on China will be much larger given the higher proposed tariff levels indicated for China and China’s much larger exposure to the manufacturing sector, with the manufacturing sector making up around 26% of China’s GDP. As growth slows, further fiscal support, monetary easing and yuan depreciation seem likely.

Potential impact of fiscal policies

The non-partisan CRFB1 estimates on its central case that if all of Trump’s tax and spending plans were implemented it would push US national debt up by around $8tr over the next ten years (a 45% of GDP increase). Already, interest payments on US government debt are larger than spending on defence or Medicare. While it is unlikely all of Trump’s proposals will be implemented, if even part of his tax cuts are passed without credible spending cuts elsewhere, there is a risk investors will view the US debt trajectory as unsustainable and will demand higher yields on government debt. In addition, the stimulatory effect of a large further fiscal expansion on an economy already growing at or above potential has the potential exert upward pressure on inflation, adding to the initial inflationary impact of tariffs.

It is of course too early to make any concrete assessments of the impact of policy given uncertainty around implementation. The Fed has taken this view, highlighting at its November meeting that until fiscal plans are known, monetary policy will remain data dependent.

However, if it looks as if even a portion of Trump’s proposed tariff and tax cuts will be implemented swiftly, all else equal, a pause in rate cuts by the Fed in Q1 2025 is plausible. An additional and related key risk to the outlook is a potential disorderly back-up in US government bond yields if the new Trump administration tries to push through tax cuts without a credible plan to pay for them. While this is not our base case, it is a key risk that needs to be watched.

Government fiscal positions back in focus

Investors should prepare for higher for longer US rates, higher public market volatility, and focus on companies’ supply chain resilience and potential direct and indirect exposures to US tariffs

Implications for investment strategy

It is too early to take any definitive views on what the new Trump administration’s economic policies will look like and their potential investment implications. However, based on what we know so far, and what we learned during Trump’s first term, there are a few key themes that stand out. The first is that higher tariffs on goods imports are likely – with China taking the brunt of the hit. The second is that tax and regulatory cuts are also likely, though it is still unclear how deep they will be and to what extent they will be offset by spending cuts. And third, that immigration controls will be tightened, likely slowing the growth of low cost labour supply.

One clear take-away from the thrust of Trump’s likely policies is that global manufacturing companies everywhere are at risk and investors will have to do detailed due-diligence on their exposures to potential supply chain disruptions, their direct and indirect exposures to the US export market and risks of increased competition from China exports diverted from the US market. Most services companies should see limited impact. However, diligence on the potential effects of tariffs on imported inputs and on business customers directly or indirectly exposed to the US goods export market will also be necessary.

In our view, in this environment investors should prepare for higher for longer interest rates, higher public market volatility and take a granular bottom-up approach to investing, with a focus on supply chain resilience and customers direct and indirect exposure to potential US tariffs. We maintain a bias towards asset light services companies with strong recurring cashflows and pricing power. Real assets and strategies with steady and resilient cashflows and inflation hedge properties, as well as strategies that are able to take advantage of market dislocations, should also perform well in this environment in our view.