The full version of this abridged interview is published in the ICG Client Lounge – our new digital portal for institutional investors to explore our global alternatives platform.

In brief

- Private equity has historically, consistently outperformed public markets over the past 20 years.

- But long-term commitments, capital calls, and limited liquidity mean private equity is often challenging for private wealth investors.

- Secondaries, by contrast, can mitigate some of the characteristic risks with private equity, offering relatively more liquid and diversified exposure to private markets.

- Success in this space, however, requires specialist teams with deep knowledge and access to the most promising opportunities.

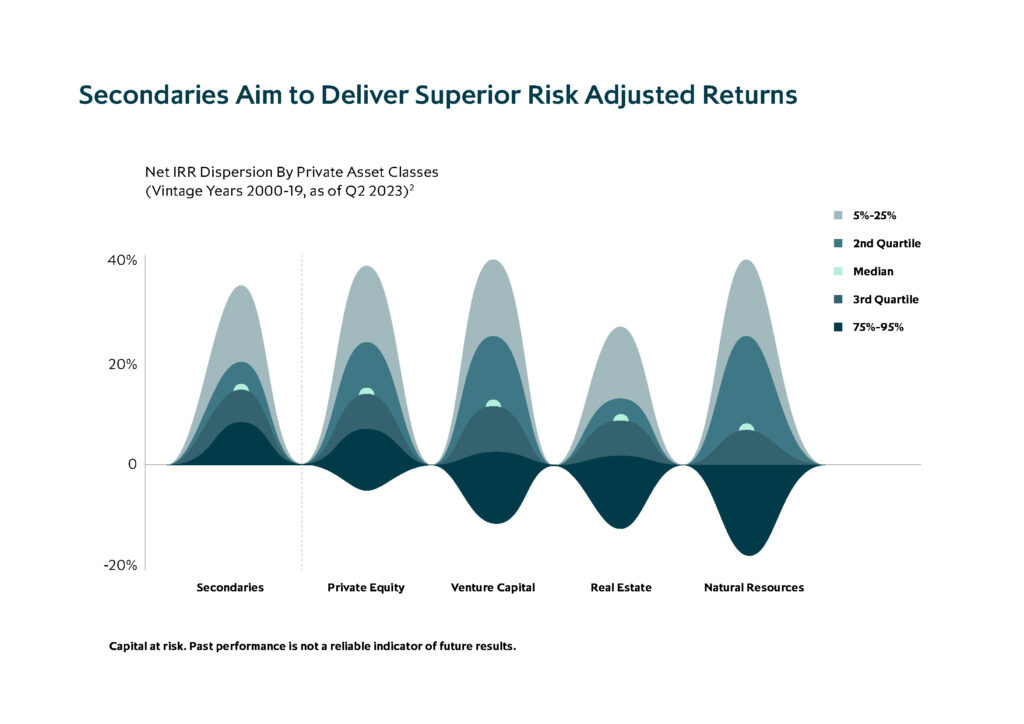

Over the past 20 years, private markets have consistently delivered higher returns compared to public markets and traditional asset classes. According to Cambridge Associates, as of Q3 2024, private equity markets delivered a 15% internal rate of return (IRR) across the past two decades, while public market equivalents counted 7.8%.[1] Elsewhere, private equity listed on Pitchbook’s North American Private Equity Index has delivered a 15.2% return compared to 9.7% by the S&P 500 over the same period.

But private equity remains largely an exclusive party. Participation in programmes has typically been closed off to all but institutional investors such as pension, insurance and sovereign wealth funds. That, however, may be changing, as private wealth increasingly finds a seat at the table.

Private equity access for private wealth

Private wealth is a broad category, ranging from high income, experienced eligible retail investors to ultra-high net worth individuals with family offices who manage their portfolios. Traditionally these kinds of investors have been limited to public markets opportunities. But with an ever-smaller pool of companies contributing to the market caps of the S&P 500 or similar stock markets, both diversification and outperformance in the public markets has become harder to achieve.

As of 2021, 87% of U.S. companies with annual revenue greater than $100 million were privately held. We believe that for private wealth investors, access to private markets is a valuable option to diversifying their portfolio.

Our conviction is that private markets offer the increased potential for enhanced risk-adjusted returns and reduced volatility over a long-term investment horizon. However, private equity isn’t suitable for every kind of investor. Such funds are often long-term commitments and highly limited in the liquidity they offer. Conventionally, the private equity investment model is designed for large, patient investors, committed to multiple capital calls for years before seeing distributions.

This is where the secondaries market comes into play. Secondaries seek to offer investors more cash efficient access to those private market opportunities, with greater relative liquidity, mitigated risks relative to private equity and PE-level return potential.

The secondaries opportunity for private wealth

The secondaries market, in its simplest form, refers to the buying and selling of pre-existing interests or assets of private equity investors.

For example: an investor commits capital to a private equity fund that purchases a stake in a private company. After time the investor in that fund may decide to sell that stake to a specialist secondary buyer. The seller gains liquidity from the sale, whilst the buyer gains a more mature asset that is in value creation mode and much nearer to liquidity.

Global secondary volume increased 4% to $112 billion in 2023, and while this is relatively small compared to the $1.3 trillion of overall private equity deal volume in 2023, the secondary asset class is growing significantly and offers private wealth an attractive asset class for private equity exposure.

“Secondary funds designed specifically for private wealth can offer access to the return potential of private equity while seeking to mitigate some of the operational challenges that private wealth investors might typically encounter when accessing alternative assets,” says Ryan Levitt, Co-Head of ICG’s LP Secondaries team.

As well as alleviating some of the factors that can make private equity unsuitable for private wealth investors, LP secondary investments can also offer a number of attractive characteristics and an advantageous risk/return profile relative to other asset classes.

“Secondaries can mitigate some of the risks applicable to investments because you can analyse the historical performance of the portfolio,” says Oliver Gardey, Head of Private Equity Fund Investments at ICG. “In addition, there is greater liquidity because at that point of investment the portfolio is already in exit mode.”

Given that the positions being acquired are more mature, secondary investments aim to offer frequent exits and cash flow events. According to Rohan Dutt, a Managing Director at Cambridge Associates, compared to other private equity vehicles, secondary strategies typically take less time to reach a distributed to paid-in capital (DPI) multiple of 1.0x, with a full return of initial capital possible – but never guaranteed – inside the first five years. Other private equity investments, such as buyouts, normally take almost twice as long to distribute paid in capital back to LPs.

Secondaries are also more inherently diversified, offering exposure to a range of assets across different industries and vintage years – helping investors enhance their overall portfolio diversification.

Success in this space, however, requires specialised skillsets to analyse large, diversified portfolios. Relationships and access to the private equity fund managers are particularly important to assess the return potential of the portfolio. Furthermore, sourcing and identifying attractive liquidity solutions for the selling LP investors is highly specialised.

The resource-intensive nature of this space creates barriers to entry that require experienced, specialised teams.

Specialising in an effort to deliver institutional level returns

ICG was a pioneer in the secondaries space, launching separate teams for LP- and GP-led secondaries with an emphasis on specialised expert investors at a time when strategies often carried out both types of deals. This commitment to specialisation means, we believe, that ICG is well positioned to create value through a differentiated approach.

Secondary investments depend on connections and knowledge across businesses and funds to identify high-quality opportunities and carry out deep due diligence. Here, the breadth of the ICG platform, with connections across different strategies, credit and mezzanine financing offerings, and co-investment strategies, offers both an information and access advantage.

As private markets continue to outperform public ones, specially designed secondaries strategies can open the door for private wealth in a way that avoids the operational challenges of traditional asset classes, while seeking to deliver accelerated portfolio liquidity.

Read the full version in the ICG Client Lounge.

Go deeper

- ICG’s key attributes and how these have evolved through the decades

- $1.6bn total commitments for ICG LP Secondaries

- Our news, insights, research and analysis

- Key terms used in this article explained in this glossary

References

[1] Source: Cambridge Associates, data as of Q3 2024. Private Equity IRR based on Cambridge Associate LLC US Private Equity Index. Private Equity PME IRR based on CA Modified Public Market equivalent (mPME) which replicates private investment performance under public market conditions. The public index’s shares are purchased and sold according to the private fund cash flow schedule, with distributions calculated in the same proportion as the private fund, and mPME NAV is a function of mPME cash flows and public index returns. mPME is a constructed index: MSCI World/MSCI All Country World Index: Data from 1/1/1986 to 12/31/1987 represented by MSCI Index gross total return. Data from January 1, 1988 to present represented by MSCI ACWI gross total return.

[2] Private equity includes buyout and growth equity; natural resources includes private equity energy, upstream energy and royalties, and timber. It should not be assumed that an investment strategy will experience comparable returns with respect to any of the asset classes shown. Such data does not reflect actual returns to any ICG client.

Past performance is not a reliable indicator of future results. Investing in private markets involves substantial risks, including the risk of capital loss. The value of investments can up as well as down.

There are no guarantees that investors will be able to redeem their investment as of any desired date. Redemptions are discretionary, subject to significant limitations and are not guaranteed.

Diversification does not guarantee a profit or protect against losses.