Key Points

- The monetary easing cycle has begun as major central banks start lowering rates

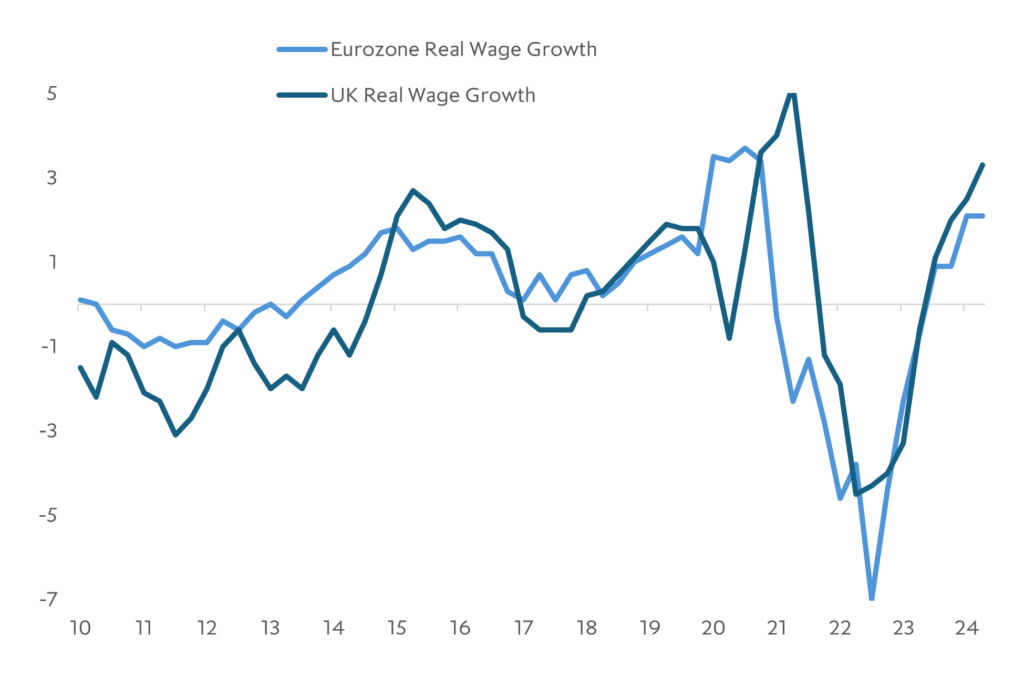

- Europe and UK economies supported by rising real incomes as energy shock fades

- US economy appears on-track for a soft landing as growth slows, but not by too much

- A constructive investing environment, but geopolitical and idiosyncratic risks are high

- In this environment we maintain a bias for less cyclical exposures, companies with predictable and resilient cashflows, and strategies that provide downside protection and can take advantage of market disruption

Overview

Summer market volatility shook markets up, but underlying economic fundamentals across most major economies support a continued constructive investing environment in our view. The spike in market volatility over the summer appears to have been driven primarily the unwinding of yen carry trades. Low liquidity and the self-reinforcing nature of the trade unwinding exacerbated the market moves. Since then, calm has returned and most risk assets have more than recouped their summer losses.

Looking forward, high frequency economic data indicates most major developed economies are seeing continued positive growth, with the economic expansion in Europe and the UK, sluggish, but on track, and early signs the US economy is cooling (but not too much). With inflation finally starting to near central banks targets, interest rate cutting cycles have begun which should support households, companies and deal flow in 2025.

Despite these positives, geopolitical risk remains high, with the Middle East and US presidential election in focus. Idiosyncratic risks also remain high, with the lagged impact of high inflation and interest rates still feeding through the system. In this environment we maintain a bias for less cyclical exposures, companies with predictable and resilient cashflows, and strategies that provide downside protection and can take advantage of market disruption.

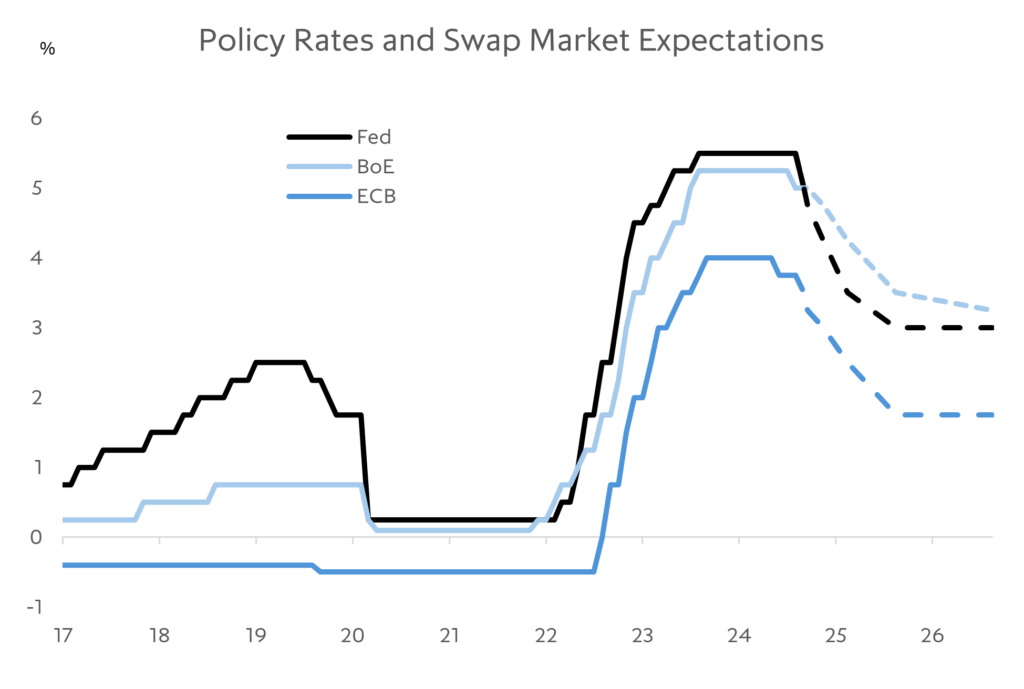

Central bank easing cycle finally underway

Watch analysis

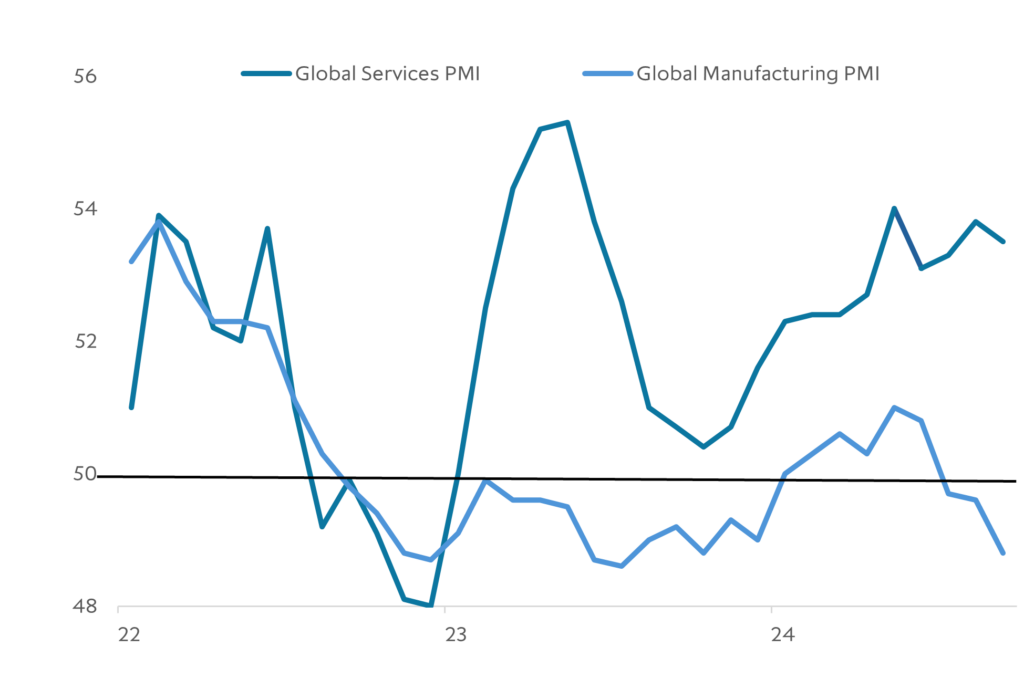

A resilient services sector is supporting global growth

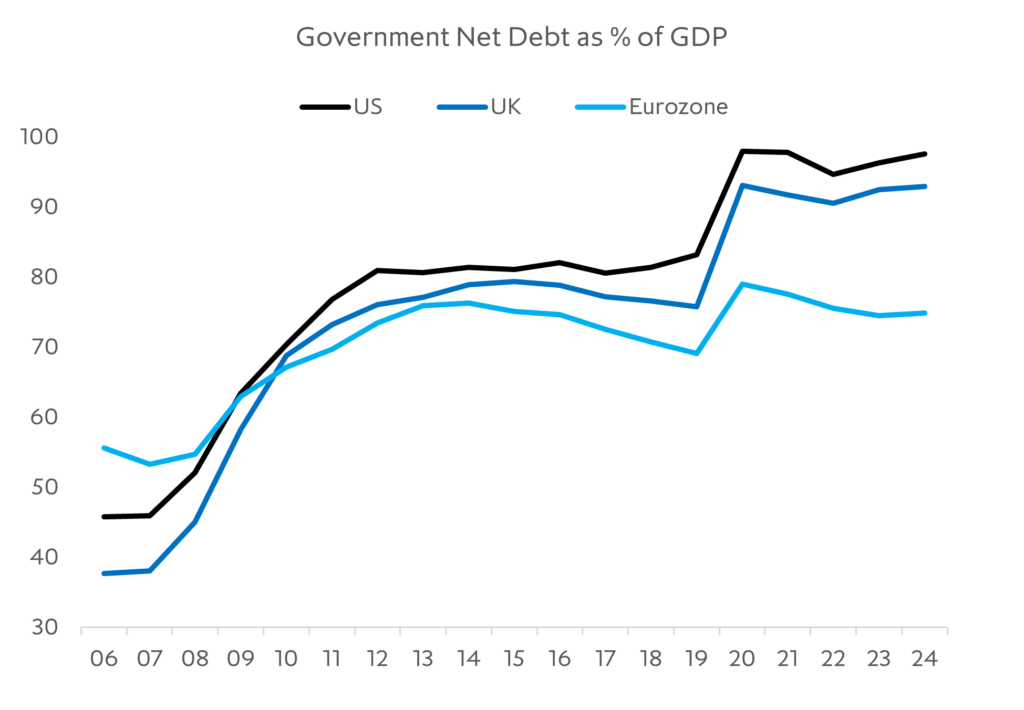

Global growth has proven to be much more resilient than expected over the past few years, as large-scale government fiscal programmes and massive central bank monetary expansion supported households and businesses through the Covid pandemic, supply chain and energy shocks. The cost has been a substantial rise in government debt burdens and a sharp increase in consumer and producer prices.

Government debt burdens have soared

While most services sectors managed to bounce back relatively quickly, the wounds to the global manufacturing sector have still not fully healed. On top of the disruptions caused by Covid and the energy price shocks, global manufacturing companies are also having to deal with rising protectionism, the threat of trade war, a sharp decline in China demand and consequent rise in excess supply as China’s economy deflates under the weight of its ongoing property crisis.

The services sector, by contrast, has continued to perform strongly. After the initial boom in demand for services following the relaxation of Covid lockdowns, services sector growth has normalised back to a lower but still healthy pace. Although there are variations at a regional and country level, generally demand for IT and business services, healthcare, entertainment and recreation, retail, travel, leisure and transportation services continue to show particular strength. Near full employment in most major developed economies, together with rising real incomes as consumer price inflation falls below still strong wage growth, should continue to support services demand going forward in our view.

A two-track global economy

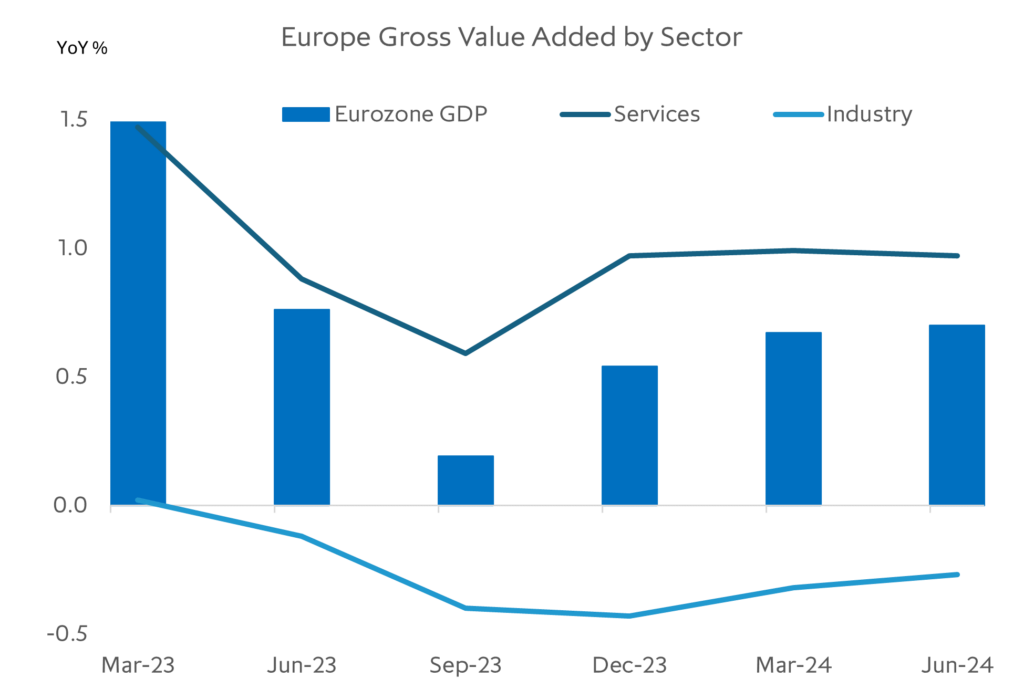

Europe and UK economic expansion on track

The Eurozone and the UK saw a healthy pick-up in economic growth in the first half of 2024. In Q3 there was some loss of momentum, primarily due to continued weakness in the global manufacturing cycle. Services sectors in most countries, however, have generally performed well. Looking forward, rising real incomes as the energy and supply shocks fade, together with falling interest rates should keep the expansion on track into 2025 in our view.

Eurozone services growth holding up well

Eurozone and UK GDP growth suffered in 2023 as industrial sectors and households struggled with the lingering effects of the sharp rise in energy costs caused by Russia’s invasion of Ukraine and the disruptions to supply chains caused by the Covid pandemic. Germany has been especially hard hit given its large energy-intensive industrial base and structural changes taking place in the auto sector.

However in 2024, outside of Germany, these effects have started to fade, allowing economic growth to start to normalise back to trend. While the Eurozone services PMI moderated in Q3 2024, underlying growth momentum in the services sector remains positive. With inflation and interest rates expected to fall further in the coming quarters, and wage growth still strong, we expect services growth to remain positive as real incomes continue to improve. In the first half of 2024 Eurozone GDP is estimated to have grown by around 0.6% and consensus forecasts are for full year growth of 0.7% and 1.3% in 2024 and 2025 respectively.

Europe and UK economies supported by rising real income growth

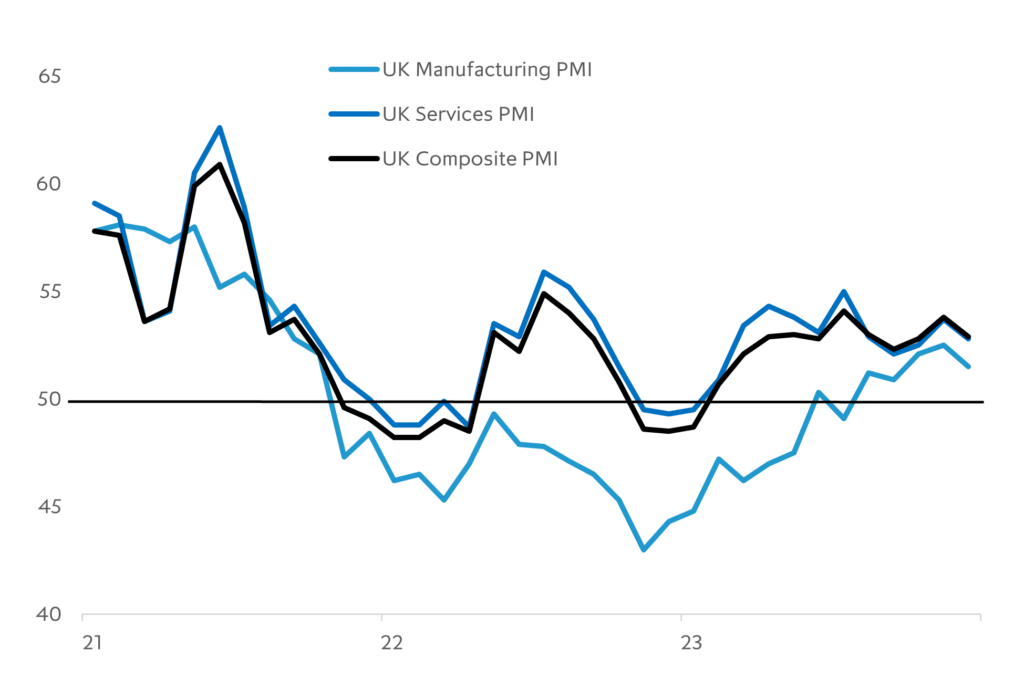

UK growth continues to surprise on the upside

In the UK, the PMIs have been surprisingly strong, with the September composite PMI rising holding at a still healthy 52.9 and the services PMI coming in at 52.8, indicating the economic expansion of the first half the year has continued into the second. UK GDP growth is estimated to have increased by 0.6% in 1H 2024 and consensus forecasts put full year 2024 and 2025 growth at around 1.1% and 1.4% respectively.

The Eurozone and the UK saw a healthy pick-up in economic growth in the first half of 2024.

UK economy holding up surprisingly well

US growth remains strong, but signs of slowing momentum

US economy continued its strong performance through the first half of 2024, with US private final demand growing by 2.6% and 2.9% in Q1 and Q2 respectively and most high frequency indicators of growth momentum holding up well. However, more recently there have been signs the economy is cooling. Over the past few months US non-farm payrolls have surprised to the downside and the unemployment rate has been creeping up. Retail sales have been slowing even as credit card outstandings have hit all-time highs. While most data points to a soft landing, and this remains our base case, soft landings are notoriously difficult to engineer, so a close monitoring of the health of the labour market, the consumer and potential ripple effects from continued stress in the regional banking sector will be critical over the next few quarters.

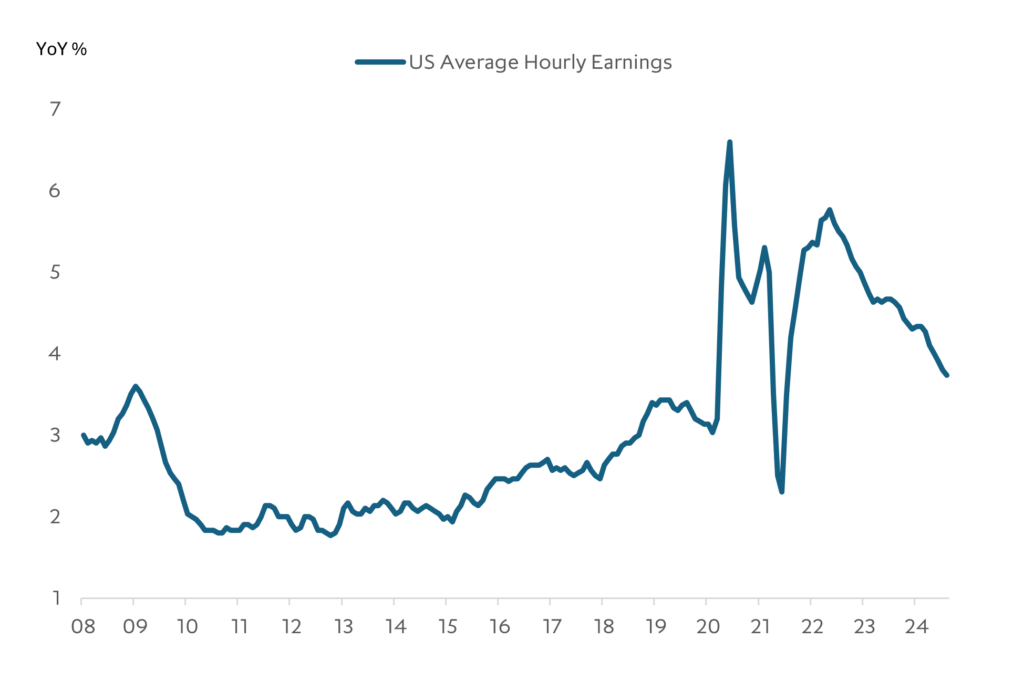

US labour market is cooling down

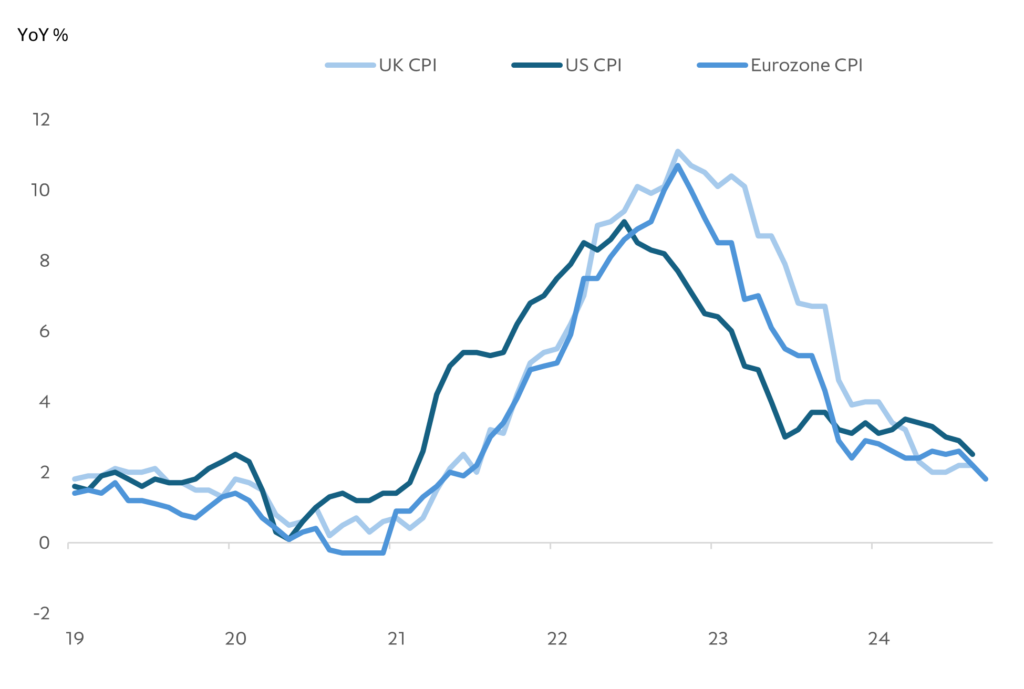

Fall in inflation allows major central banks to start rate cutting cycles

With US inflation finally coming into the range of the Fed’s 2% target and employment data cooling, the Fed finally commenced its much-anticipated easing cycle with a larger than expected 50bp cut to its benchmark rate in September.

Headline and core CPI came in at 2.4% and 3.3% respectively in September. While domestic demand, as highlighted above, is still relatively strong, signs of cooling in the labour market and lead indicators pointing to further declines in wage growth and shelter inflation, should allow the Fed to steadily lower rates in the coming quarters. Swap markets are currently pricing another 75bp of cuts by year end and a further 100bp of cuts in 2025. While still resilient growth and sticky services inflation indicates to us that swap markets may again be getting ahead of themselves, the trend towards lower rates seems clear.

While we think systemic risks are low, we think idiosyncratic risks remain higher than normal.

Inflation nearing central bank targets

In Europe, with underlying inflation pressures easing and growth momentum moderating, the ECB implemented its first 25bp rate cut in June and followed up with a second cut in September. We believe this marks the start of a measured but extended easing cycle as inflation nears its medium term target of 2%. Current swap market pricing implies the ECB’s benchmark rate will fall from the cycle peak of 3.5% to around 2.0% over the next year.

In the UK, with economic growth more robust than the Eurozone and underlying services inflation proving stickier, the BoE waited until August before implementing its first rate cut, lowering its benchmark rate 25bp to 5%. Swap markets are currently pricing in just under two more 25bp rate cuts by the BoE this year and around another 100bp next year.

A constructive investing environment, but idiosyncratic risks still high

If this macro environment holds, we think the overall investing environment will remain constructive. However, the lagged impact of high interest rates is still feeding through segments of the market and for some companies the wounds from the Covid pandemic and energy price crisis have not fully healed. Therefore while we think system level risks are quite low, we think idiosyncratic risks remain higher than normal. In this environment we maintain a bias for less cyclical exposures, companies with predictable and resilient cashflows, and strategies that provide downside protection and can take advantage of market disruption.