Key points

- Banking turmoil likely to weigh on growth. The failure of Silicon Valley Bank (SVB) and the ripple effects through US regional banks, combined with the collapse in confidence in Credit Suisse and the emergency take-over by UBS, has added to already high economic and financial uncertainty, will likely weigh on growth and keep market volatility high in the coming months in our view.

- But systemic financial crisis is unlikely. Swift moves by regulatory authorities and central banks to stem contagion, crisis management tools developed since the 2008 financial crisis and the strong financial positions of major money centre banks, means a systemic financial crisis of 2008/09 proportions is unlikely.

- Banking sector consolidation and tighter credit conditions ahead. However, deposit flight and likely more restrictive regulatory controls on small and medium-sized banks in the US will likely lead to banking sector consolidation and reduced credit provision in the coming quarters. It is too early to judge how large an impact the banking turmoil will have on the economy, but Fed Chair Powell said he thought it could be the equivalent of “a rate hike or perhaps more than that”.

- Operating environment for companies to become more difficult. The events of March are a vivid example of how the sharpest rise in major market interest rates since the 1980s can (and likely will continue to) have unpredictable consequences. Looking into the rest of 2023, the operating environment for many companies will likely become more difficult, with slowing economic growth weighing on top-lines and the reduced ability to pass on higher input and interest costs to increasingly constrained consumers, pressuring margins.

- China opening, lower energy prices, swifter rate cuts to provide positive offsets. It is not all bad news, however. China reopening following the removal of Zero Covid restrictions will likely partially offset the weight on global growth from higher interest rates and tighter credit availability, as will the sharp fall in energy prices. The recent bank upheaval will also likely reduce the peak level of rates and incentify a swifter reduction in rates once core inflation likely starts falling more quickly in the second half of the year.

- Sector and company performance differentiation to remain wide, bringing opportunity for longer-term bottom-up investors. While company fundamentals will likely weaken at an aggregate level, we think the deterioration will be highly sector and company specific, with companies in the less cyclical, less energy-intensive sectors continuing to outperform. Consolidation within sectors will also likely bring opportunities for growth-enhancing acquisitions and partnerships.

- The less cyclical sectors private investors tend to be exposed continue to outperform. Sectors such as healthcare, technology and software, communications, education, consumer staples, infrastructure and companies helping the green transition are likely to outperform over the coming quarters. On the other hand companies exposed to consumer discretionary spending, parts of the real estate sector and other cyclical and interest rate sensitive sectors are likely to experience intensified pressure.

- Private capital to play increasingly important role filling the funding gap. With market volatility reducing companies’ access to public market funding and bank credit becoming increasingly scarce, private capital providers with long-term locked-in institutional funding, large stores of dry powder and long-term investment horizons, will likely play a growing role helping to fill the widening funding gap. Aiding this trend, the historically high returns offered by private debt are likely to continue to attract long-term institutional funds, supporting the continued rebalancing of funding away from banks towards private capital providers.

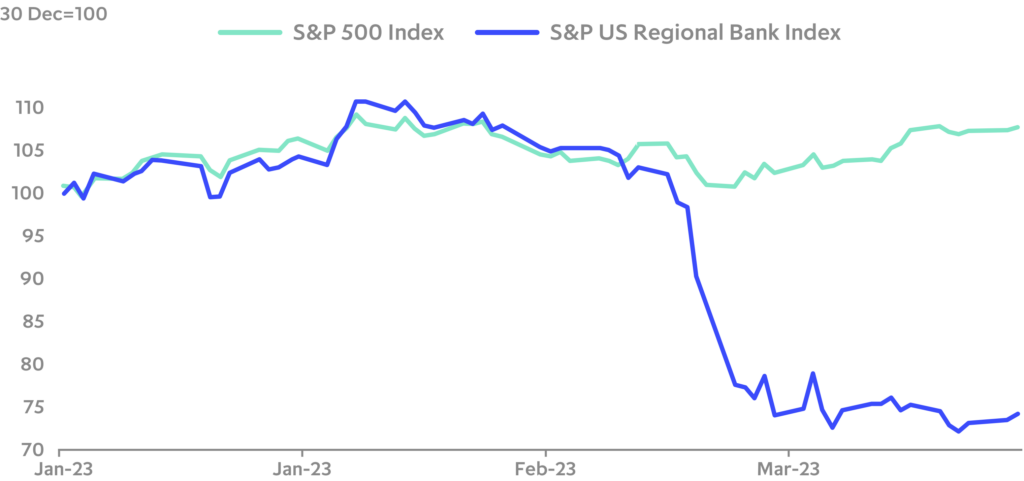

US Regional banks under pressure

Banking turmoil: What happened?

The failure of Silicon Valley Bank (SVB) and the ripple effect through US regional banks forced the Fed to resort to extraordinary measures, including the closure of SVB and Signature bank and the opening of a new financing facility, to stem further contagion. The loss of confidence in US regional banks, along with negative comments from a major shareholder and other idiosyncratic concerns were enough to create a crisis of confidence in long- suffering Credit Suisse, forcing Swiss authorities to cobble together an emergency take-over by UBS over the course of a weekend.

Intervention has calmed markets for now

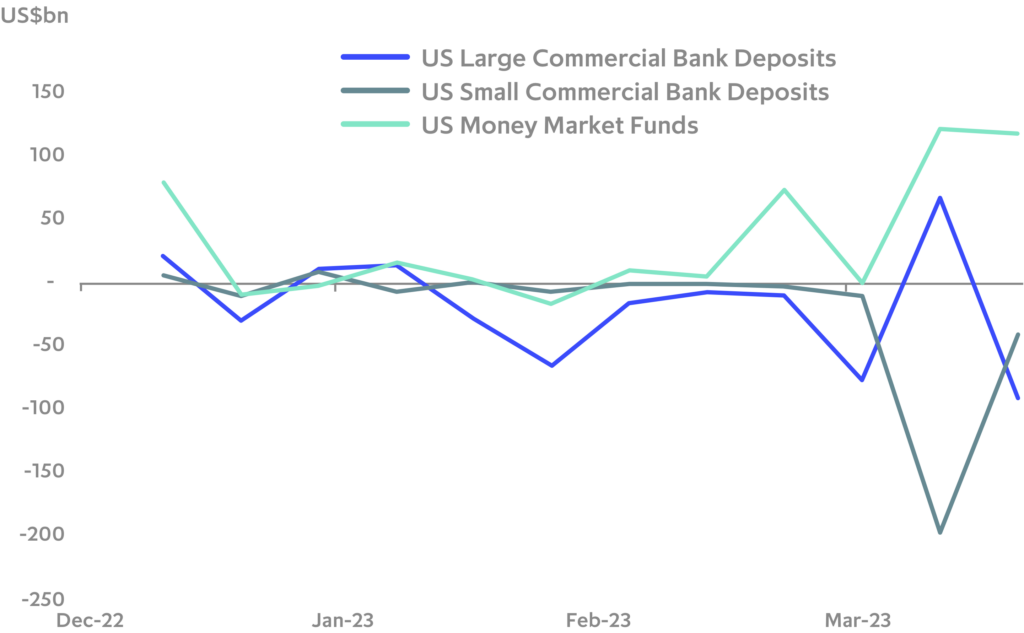

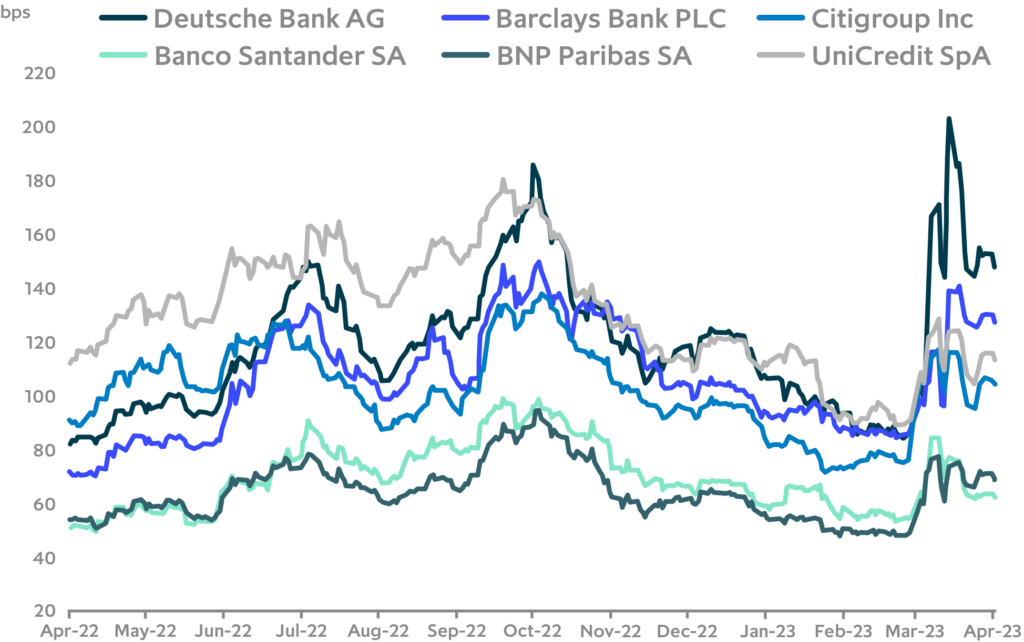

While measures taken by central banks and regulators have calmed markets for now, at the time of writing, US deposit outflows from smaller banks to larger banks and into money market funds appears to have continued, though at a slower pace than early in the crisis, and credit default spreads of a number of major banks remain elevated relative to recent history (though still well below 2008/09 levels).

US small bank deposit flight appears to be slowing

Banks CDS spreads have widened, but remain well below 2008/09 levels

The ability of US banks to borrow from the Fed’s discount window and the newly created Bank Term Lending Program (BTLP) with collateral such as treasuries and other qualifying assets valued at par, should solve the immediate mark-to-market problem behind the recent loss of confidence in regional banks. But depositor confidence is notoriously difficult to restore once lost, and continued deposit withdrawals from regional banks could force larger-scale intervention by authorities, including some form of additional deposit insurance and/or forced consolidation across the sector.

Growth impact should be small if contagion remains contained

To the degree the turmoil is contained to regional banks and any sector consolidation is done in an orderly manner, the impact on the US (and global) economy should be relatively small and sector specific in our view. Early estimates of the potential impact on US growth are in the range of .25 to 1 percentage points of GDP and around half that magnitude for the Euro Area. Of course, given the fluidity of the current situation, there is very high uncertainty around these estimates.

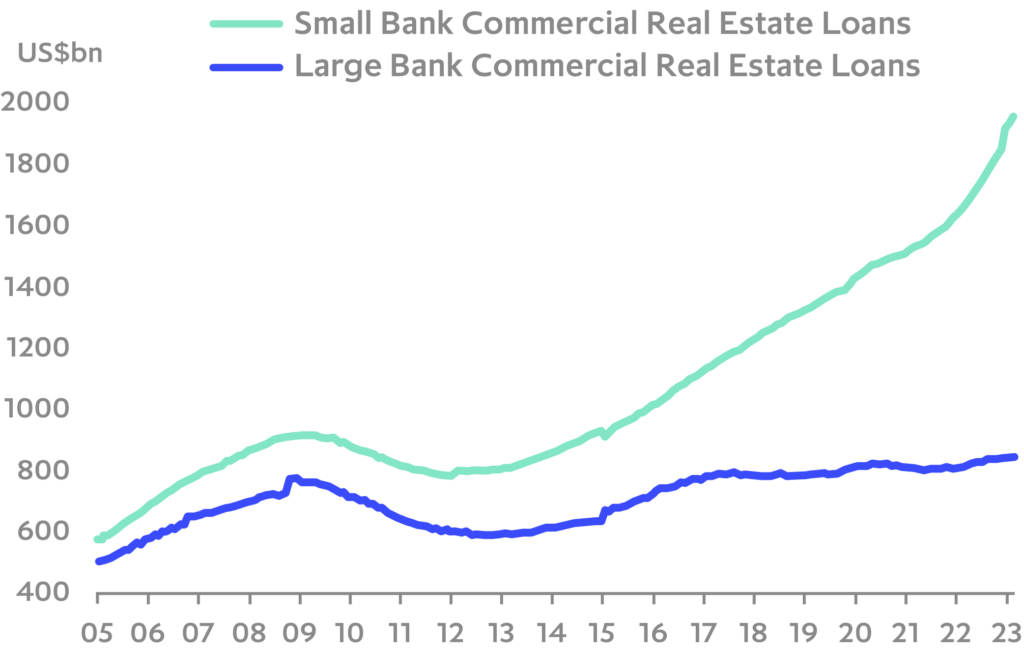

US commercial real estate remains a potential vulnerability

One area that could still spark further disruption, however, is US commercial real estate (CRE) – particularly the office sector – due to high dependence on credit from smaller banks and already weak fundamentals. There is a risk the decline in regional banks’ deposits, combined with balance sheet losses on existing CRE loans, leads to a self-reinforcing cycle of a reduction in credit to the CRE sector putting more pressure on commercial real estate, which then causes further losses on CRE loans, forcing a further reduction in lending and so on.

While problems in the commercial real estate sector have the potential to further damage confidence in regional banks and to disrupt markets, the Fed and regulatory authorities are well aware of these risks and will likely intervene quickly and forcefully to prevent wider contagion if needed.

Over 70% of US commercial real estate loans come from small banks

Systemic financial risks remain low

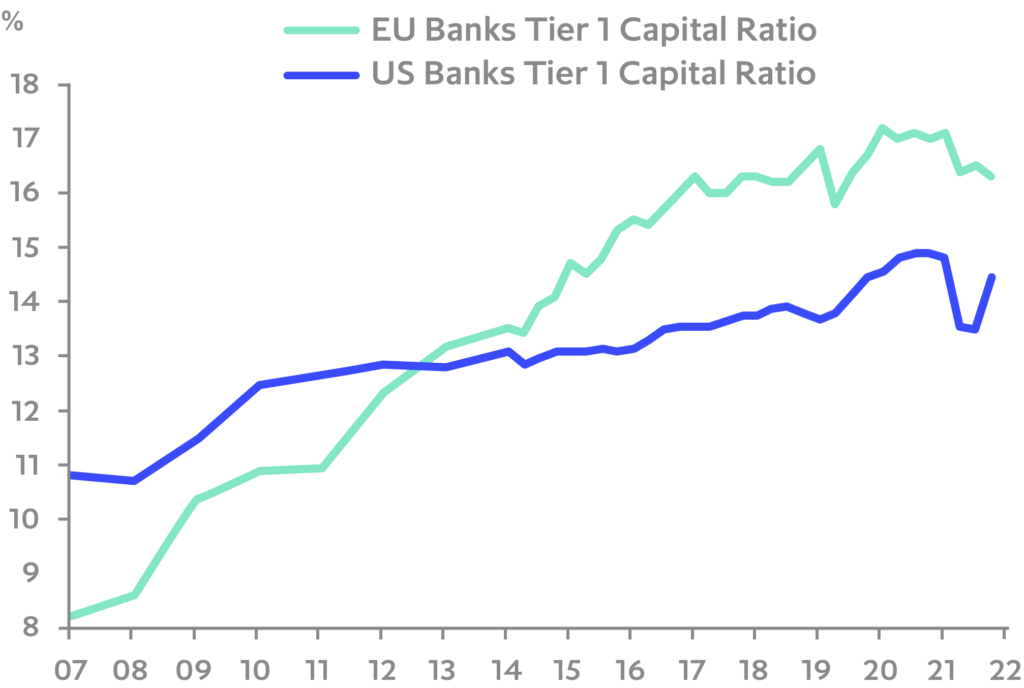

Despite idiosyncratic and sector specific risks, at an aggregate level, US, Eurozone and UK banking systems are substantially stronger than they were in the run up to the 2008/09 global financial crisis and systemic risk is low we believe.

Much stricter prudential requirements over the past fifteen years have substantially boosted balance sheet strength and liquidity buffers, lending standards have improved, and regular stress tests of large banks have helped catch potential systemic risks early. Therefore, while some smaller banks may continue to feel pressure, and consolidation and further regulatory intervention in the US small and medium-sized banking sector seems likely, the risk of a broader systemic financial crisis involving the major money centre banks remains low in our view.

System-wide bank balance sheets remain strong

Economic implications: Where to from here?

US: Slower growth ahead, nearing peak rates

The upheaval in the US regional banking sector is a clear example of “something breaking” as the Fed tightening cycle passes its one-year anniversary.

The dilemma the Fed faces is that while it is acutely aware of the potential for further unintended consequences from additional interest rate increases, most recent inflation readings indicate that core services inflation has not yet been fully brought under control. What should ease the Fed’s dilemma, however, is that the recent shock to US regional banks and financial markets will likely do some of the tightening work for them.

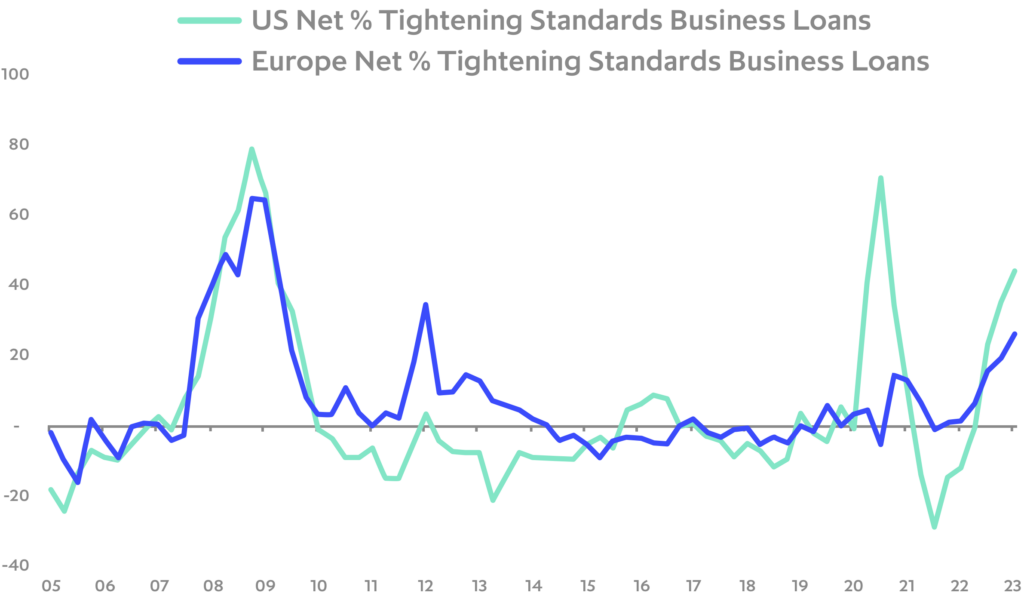

Bank credit standards tightening, taking tightening pressure off central banks

It’s too early to assess how the bank and market upheaval will feed through the economy, but early estimates put the potential impact as equivalent to at least 25bp to 50bp in Fed rate hikes. With the pre-upheaval Fed dot plot indicating peak rates of around 5.25%, if the tightening impact of the recent bank turmoil proves correct, the Fed should nearly be done.

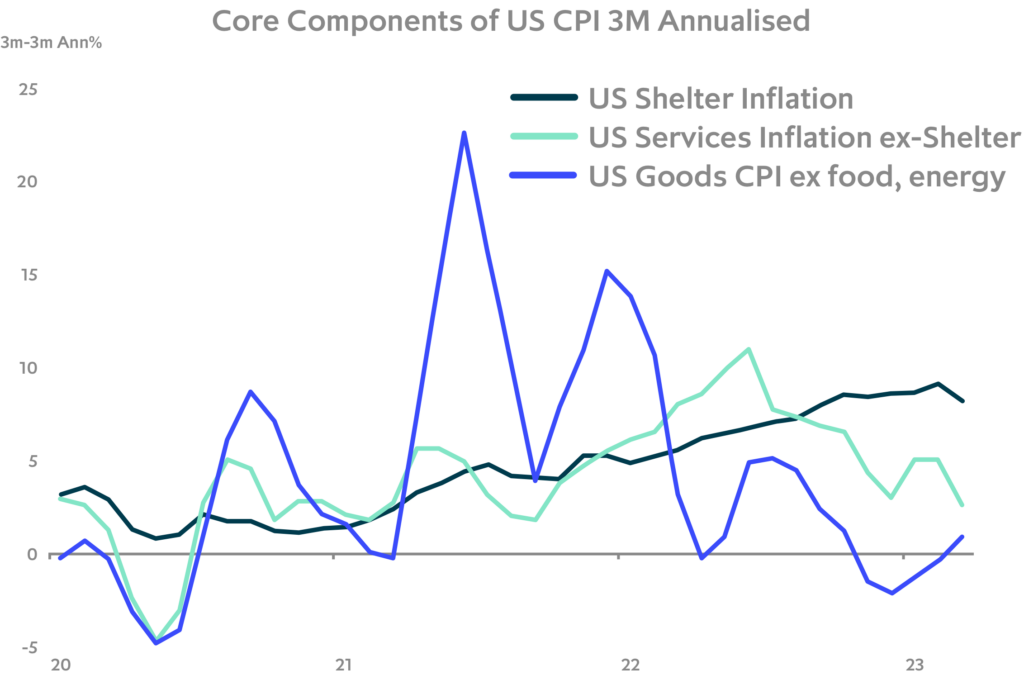

US services inflation ex-shelter is trending down

US economic growth has proved to be much more resilient to higher interest rates, energy and other input costs than many expected, as the rundown of savings built up during the Covid period and release of pent-up demand has supported consumer demand – particularly for services. GDP growth came in at a healthy 2.6% in Q4 2022 and is tracking around 1.6% in Q1 2023. The big question going forward is whether the US economy’s resilience to higher rates and recent bank and financial volatility is sustainable or if the impact is just delayed. We suspect the effects of financial tightening will become much more evident in the coming quarters, with cyclical and interest rate sensitive sectors coming under pressure.

However, with employment markets still healthy relative to previous cycles and consumer balance sheets still strong, barring a much larger domestic or external shock, we think the slowdown we remain highly sector focused, and a broader deep recession is likely to be avoided.

Europe and UK: Limited impact so far

Europe and the UK have so far been less affected by the banking turmoil than the US. While bank securities prices and credit spreads have been negatively impacted by US regional bank disruption and the crisis at Credit Suisse, the direct impact on system-wide financial confidence has so far been limited.

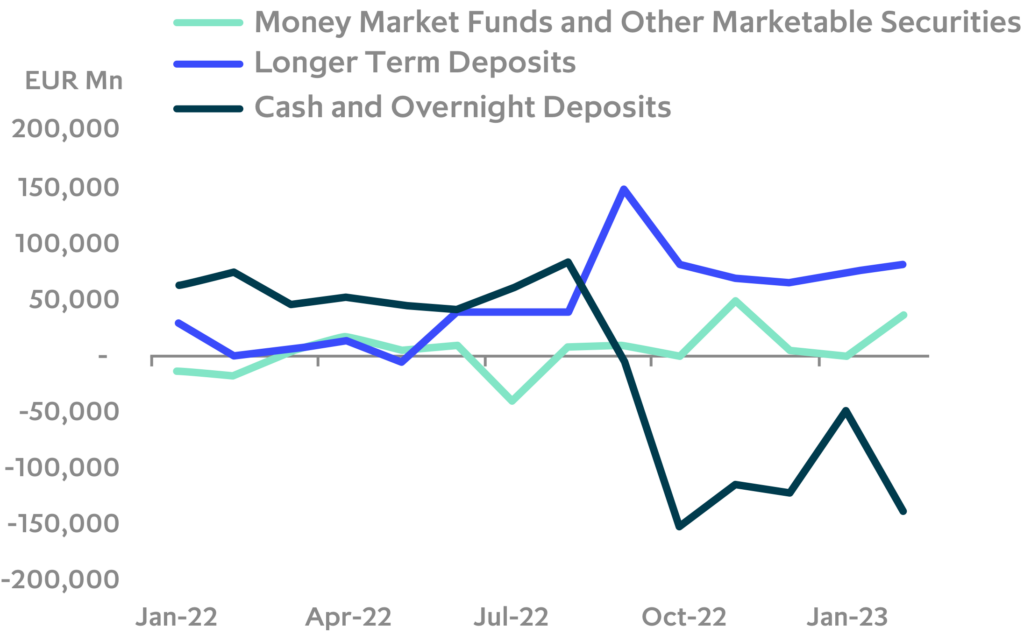

In Europe there has been a shift from cash and overnight deposits into longer term deposits, but this has been driven by the much higher relative return on term deposits since the ECB began tightening last year, not by the recent bank turmoil. And, so far, there does not appear to have been the kind of dramatic shift of depositors out of small banks and into large banks and money market funds seen in the US.

Eurozone term deposits rise as interest rates increase

Post the 2008-09 global financial crisis and the 2010-12 Euro crisis, Europe and the UK built new financial system support tools and put in place more stringent supervision that has substantially strengthened their financial systems. Supervision of smaller banks has been more stringent than in the US, banks across the size spectrum have been forced to build strong capital positions, have high liquidity coverage ratios and interest rate hedging is more prevalent than in the US.

That doesn’t mean that the banks in Europe and the UK are immune to further turmoil, but it provides some confidence that any bouts of banking sector related contagion will be able to be effectively contained by the central banks and regulators.

ECB has further tightening to do, but rate expectations should fall in 2H 2023

Falling energy and food price inflation should lead to a sharp drop in Europe’s headline inflation rates over the next few months. Core inflation, however, has been sticky, with latest data showing a continued acceleration through March. Looking forward, the lagged impact of lower energy prices on core input prices together with the clearing of most supply chain bottlenecks and cooling property markets, should start feeding into the core numbers in the coming months. The wild card is wage growth, with pandemic-driven distortions to labour market supply and services demand keeping labour markets tighter for longer. But as consumer demand slows, so too should labour demand, putting downward pressure on wages and services inflation. Therefore, while the ECB will likely try to get in a few more rate hikes in the next few months (barring further major financial upheaval), by 2H 2023 core inflation and rate expectations should be falling in our view.

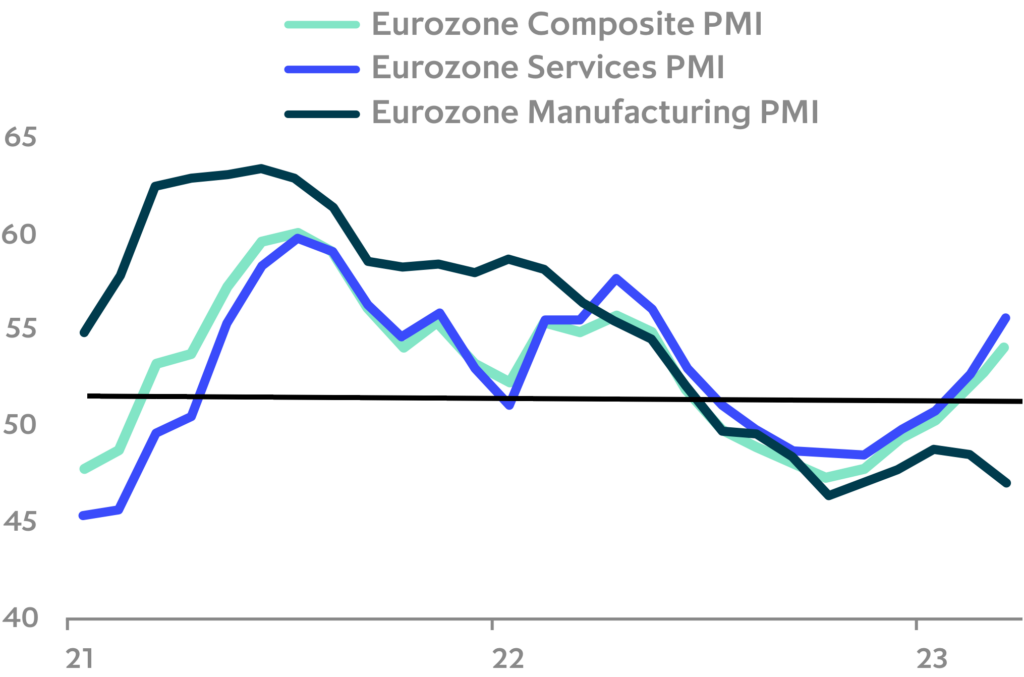

In terms of growth, Europe has surprised to the upside through most of 2022 and into 2023, with strong fiscal responses to the energy shock, tailwinds from post-pandemic reopening keeping demand for services strong, and sharp declines energy prices – natural gas in particular – supporting growth and sentiment through the winter months. Europe’s purchasing manager indexes have rebounded steadily from their October lows, with the Eurozone composite index rising to 54.1 (above 50 indicates expansion) in March, its highest level since May 2022.

Services have been the main growth driver, with entertainment, recreation, retail, travel and food services seeing the strongest demand as consumers release pent up demand built up during the pandemic. A strong jobs market has helped boost consumer confidence, which together with high saving, has supported consumption despite the decline in disposable income as inflation has increased.

Europe services growth has remained strong

Slower Europe growth ahead, but moderate relative to previous cycles

While the lagged impact of higher interest rates, recent financial volatility and fading re-opening tailwinds are likely to weigh on growth going forward, the region will be supported by the easing provided by the recent fall in energy prices and is likely to be a key beneficiary of China’s economic re-opening following the removal of its zero-Covid policy.

Therefore, while we expect growth to slow in the coming quarters, assuming the current financial sector turbulence remains contained and external geopolitical and economic conditions do not deteriorate substantially, the downturn is likely to be moderate relative to previous cycles . However, that does not mean there won’t be distress in some segments of more interest rate and cyclically sensitive sectors, putting a premium, as always, on rigorous bottom-up asset selection.

BoE: First in, first out?

The BoE was the first major central bank to start raising interest rates and it appears the most likely to stop first as well. Although coming from a high level, core CPI has been trending down in recent months and both the BoE and ONS are forecasting sharp declines in CPI in the coming months. In addition, UK domestic demand has been weakening, with retail sales volumes still in negative territory relative to 2022 levels. Weak growth combined with falling housing prices give the BoE incentive to stop tightening as soon as it feels it has core inflation sustainably moving in the right direction. Most indications are we are near that point.

UK sluggish growth ahead

The UK has seen a particularly sharp shock from higher energy prices partly due to its high reliance on natural gas as an energy source and partly because its household energy pricing mechanisms meant a large part of price increases went quickly through to end-users. Mortgage rates have also risen sharply as the BoE has raised rates and with around 40% of mortgages on variable rate or 2 year fixes the impact has come through more quickly than Germany, France and the US where longer term fixed rates make up the bulk of the market. Although UK GDP managed to eke out an 0.1% rise in Q4 following a small contraction in Q3, it remains the only major developed economy not to have fully recovered to pre-Covid levels.

Despite the relative weakness of the UK economy, strong consumer, financial and corporate balance sheets mean systemic risks are low and any recession should be relatively mild in our view. As the fall in energy prices reduces the drag on household disposable income, recent fiscal easing feeds through to the economy and market interest rates decline, some of the worst of the drag on economic growth should ease.

Implications for private market investors

Low allocation to cyclicals limits downside risks

While company fundamentals will likely weaken at an aggregate level, we think the deterioration will be highly sector and company specific, with companies in the less cyclical, less energy-intensive sectors continuing to outperform. Sectors such as healthcare and biotech, technology and software, communications, education, consumer staples, infrastructure and companies facilitating the green transition are likely to hold up well on a relative basis in the coming quarters.

There are also likely to be pockets of distress, with some companies exposed to consumer discretionary spending, parts of the real estate sector and other cyclical and interest rate sensitive sectors in particular seeing continued pressure.

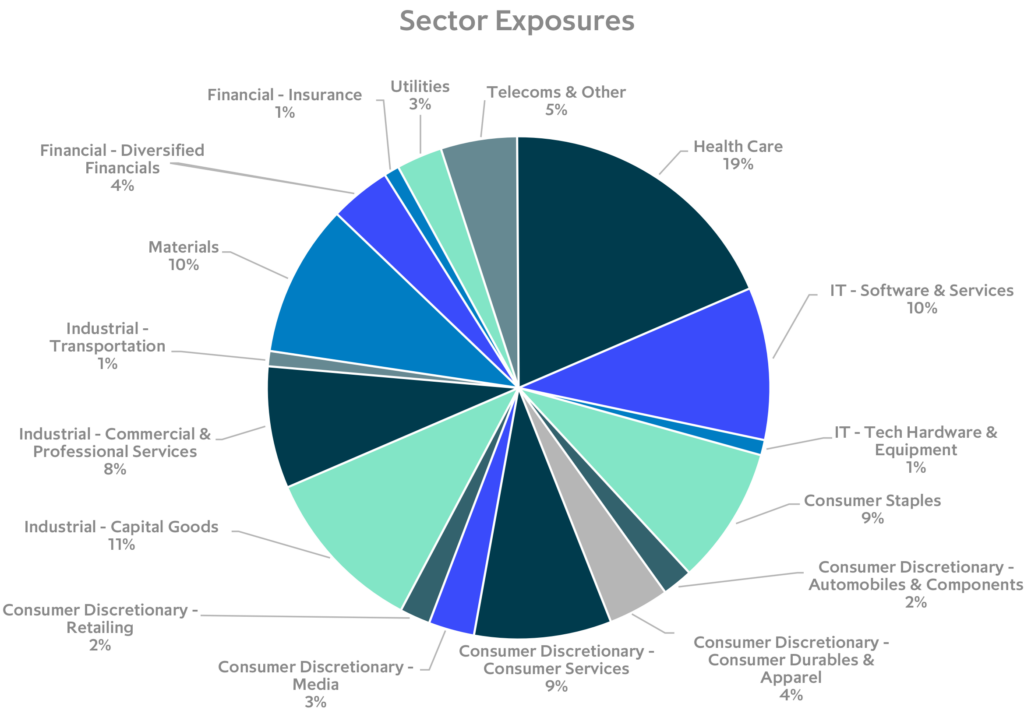

Private market investors are well-positioned in this environment, with the ICG private company database indicating low exposure to most cyclical sectors (see chart below). This held most private market investors in good stead through the Covid pandemic and should do so again in our view as we move into a more difficult operating environment in the coming quarters.

Private company sector allocation

Well positioned to fill the funding gap

With high market volatility, restricting companies access to public market funding, and banks rapidly pulling back on lending, private capital providers will likely, as they have in the past, provide a useful countercyclical source of capital for companies.

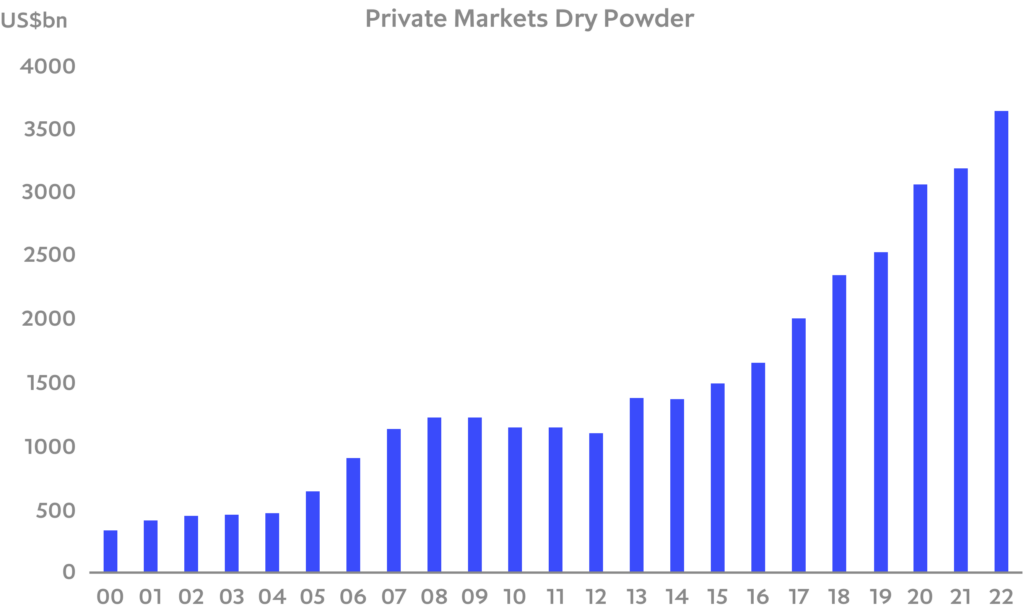

With large stores of dry powder, medium to long-term investment horizons, long term sources of locked-in institutional funding and the ability to provide flexible capital in size, private capital providers are in a strong position to help fill the growing funding gap in the coming quarters in our view.

Aiding this trend, the historically high returns offered by private debt are likely to continue to attract long-term institutional funds, supporting the continued rebalancing of funding away from banks towards private capital providers.

Private markets dry powder at a record high