Overview:

- Slower growth ahead, but structural factors should limit the depth and duration of the slowdown. Recessions are likely in most developed economies in the next few quarters but, barring a major escalation of the Russia-Ukraine war or other unforeseen shock, in most cases they are likely to be relatively shallow and highly sector specific.

- Solid fundamentals and strong policy response provide downside protection. Despite the headwinds of higher rates and prices, there are a number of structural factors that should cushion Europe and the UK from the fall-out from the energy price shock. These include: 1) strong household balance sheets (including record levels of household savings), 2) strong corporate balance sheets, 3) well capitalised and stress-tested banks, 4) highly supportive fiscal policy, 5) Faster than expected build-up of natural gas reserves.

- Inflation should fall in the latter part of 2023, taking pressure off interest rates and reducing the squeeze on disposable incomes as higher energy prices roll out of inflation calculations (energy and food have contributed to nearly 50% of Eurozone inflation). Other input costs will also likely moderate as supply chain bottlenecks and labour markets ease and property markets cool. This should allow Euro rates to remain well below US rates and alleviate pressure on domestic demand later in 2023.

- Large-scale fiscal support programs in Europe and the UK should help cushion households and businesses through the worst of the energy price shock. Governments in Europe and the UK are acting aggressively to protect households and businesses from higher energy costs through varying combinations of energy tax cuts, subsidies, direct payments and price caps ranging from 2% to 8% of GDP.

- The slowdown in growth is likely to be highly sector specific, with less affected sectors continuing to outperform despite a broader slowdown. Less cyclical and less energy-intensive sectors such as healthcare and biotech, technology and software, business and financial services are likely to hold up relatively well over the next quarters in our view. Businesses directly involved in or facilitating the acceleration of the green energy transition are likely to see significant tailwinds.

- Europe is not homogeneous, country performance will vary widely. Performance will range widely depending on countries’ sector compositions, energy and interest rate exposures, regulatory and pricing regimes and policy responses among other factors. One can’t take a broad-brush approach to investing in Europe.

- An environment well-suited to private market investors. As during the pandemic, market disruption and wide performance dispersion at a country, sector and sub sector level brings opportunity for investors with medium to long-term investment horizons, strong bottom-up analytical skills, local knowledge, flexible capital and close working relationships with investee companies. With public market volatility likely to remain high and banks continuing to retrench, this environment should be particularly suited to private market investors in our view

Where to from here?

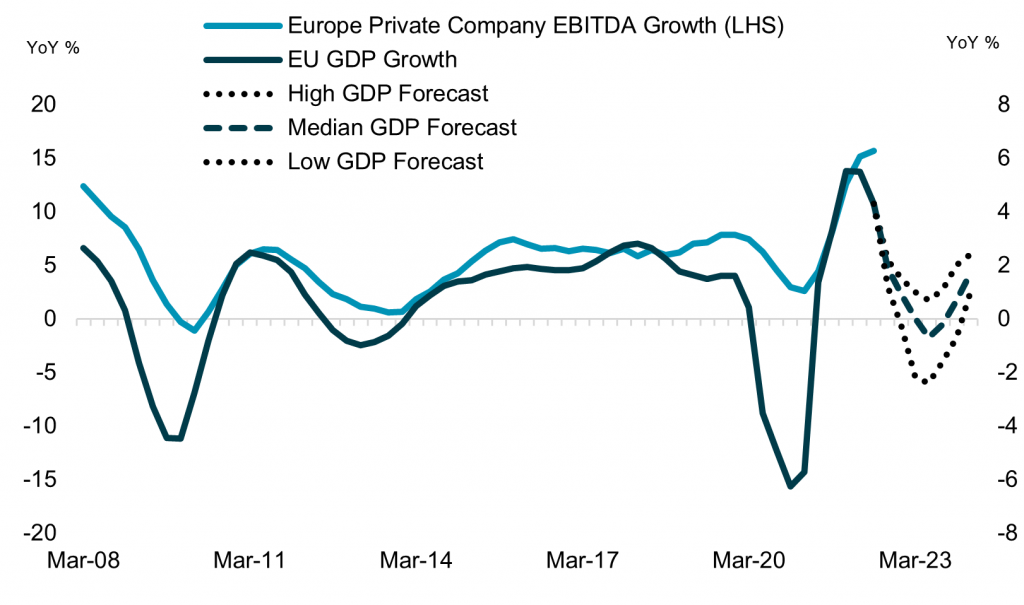

Source: ICG Private Company Database and Bloomberg. Data 4QMA to Q2 2022. Forecasts are Bloomberg consensus high, low and median GDP forecasts as of 26 October 2022.

Europe’s economies have outperformed expectations through most of 2022, showing surprising resilience despite the ongoing war in Ukraine, the sharp rise in energy prices and higher interest rates. In the first nine months of the year, the Eurozone and UK economies grew by an average of around 4% in real terms over 2021 levels, continuing the recovery that began in 2021.

This has been reflected in strong company performance, with Euro Stoxx 600 ex energy earnings up an estimated 12% in Q2 2022. Europe private company earnings growth has also been strong, with median earnings of the companies tracked by ICG’s private company database up 16% over the same period and leverage and interest coverage ratios holding at comfortable levels.

The question in most investors’ minds, of course, is where do we go from here?

In our view, while the next few quarters will be challenging and, along with the US, a number of countries will fall into recession, there are structural and policy factors that should limit the depth and duration of the coming slowdown. These include strong household, company and bank balance sheets, low unemployment, large-scale fiscal support programs and much larger than expected stores of natural gas coming into the winter months.

Also, critically, we think the slowdown will be focused in a few key sectors, with weakening headline GDP growth trends masking highly varied performance at a sector and sub-sector level. As we saw during the worst of the pandemic period, investment performance will likely depend more on sector exposures than country exposures.

Therefore, while we think the next few quarters will be more challenging, wide performance variation at a country and sector level is likely to bring opportunity for investors with strong local knowledge, a bottom-up approach to investing and medium to long-term investment horizons.

Growth and earnings slowdown ahead

Despite the disruptions caused by Russia’s invasion of Ukraine and China’s zero-Covid policy, the US, Europe and the UK economies proved to be more resilient through the first part of 2022 than most headlines would indicate. While consumer sentiment has fallen sharply since the invasion as higher energy and other prices have eroded real spending power, most hard indicators of growth and employment held up better than expected through the first part of the year.

It seems likely, however, that growth will slow more quickly in the coming months as the lagged impact of higher interest rates and inflation feeds through to consumers and businesses, and the initial momentum from economic re-opening starts to fade. Slower economic growth, earnings downgrades, front-loading of interest rate hikes by major central banks and tight natural gas supplies over the winter months, will likely keep uncertainty and market volatility high in the coming months.

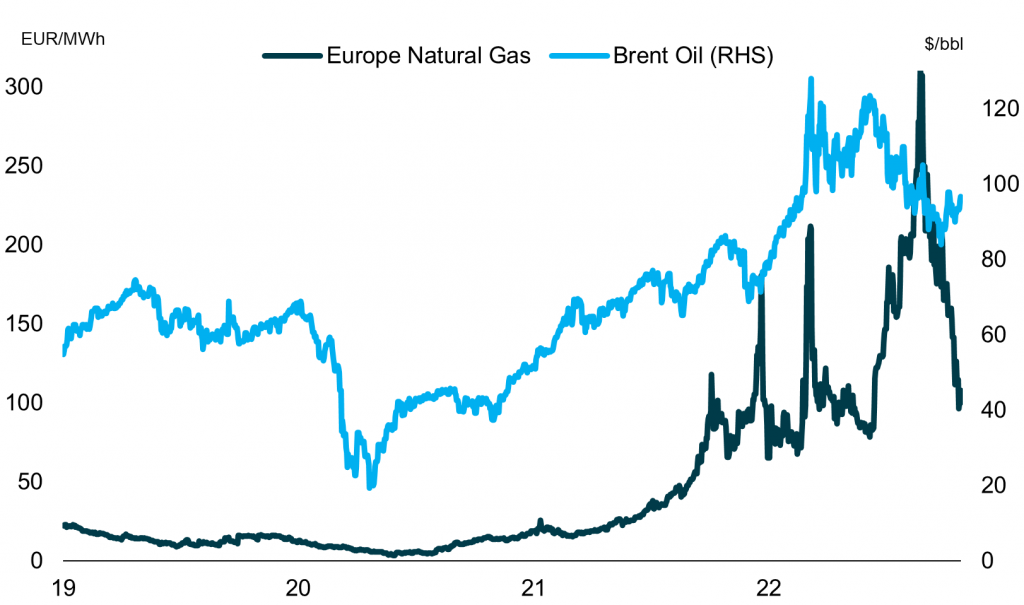

Energy prices down sharply from highs

Structural supports and large-scale fiscal intervention should cushion the fall

There are, however, a number of offsets that are likely to help cushion economies during this adjustment period.

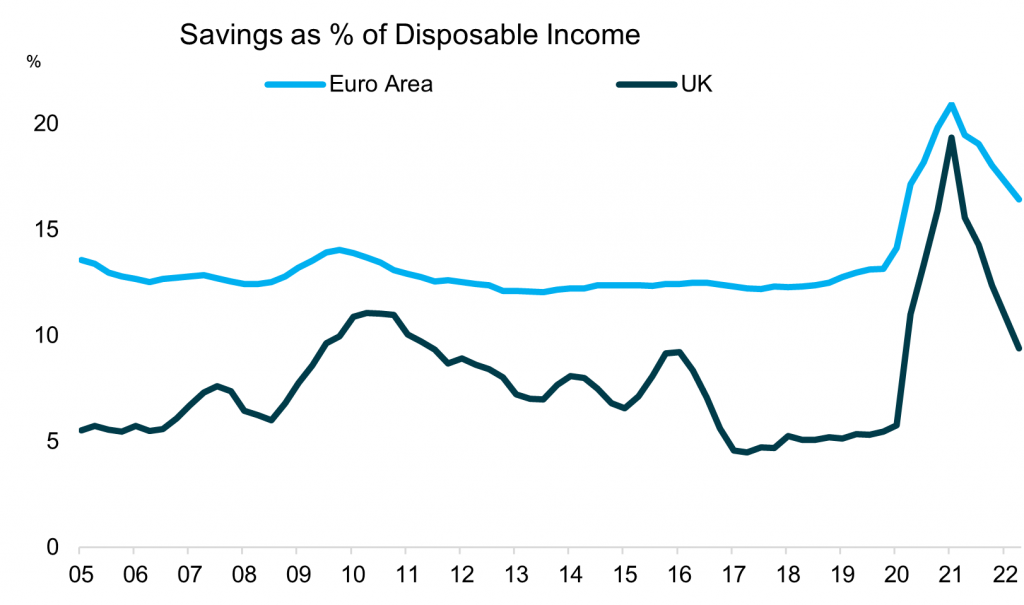

Strong household balance sheets

The first is that household balance sheets enter this period in healthy shape. The combination of generous government support packages and limited ability to spend during the worst part of the Covid-19 pandemic caused household savings to rise to record levels.

Although spending on non-essential goods is likely to slow as high energy, food and other prices eat into disposable income in the coming quarters, the large store of saving built up during the pandemic will likely be tapped to shore up and help smooth consumption over the period.

Bank for International Settlements (BIS) data shows that household debt service ratios are at or near historic lows.

Job markets are also strong, with unemployment rates in the US and UK at or below pre-Covid lows and the unemployment rate in the Eurozone its lowest on record.

Large stores of household savings to tap

Company balance sheets are also strong

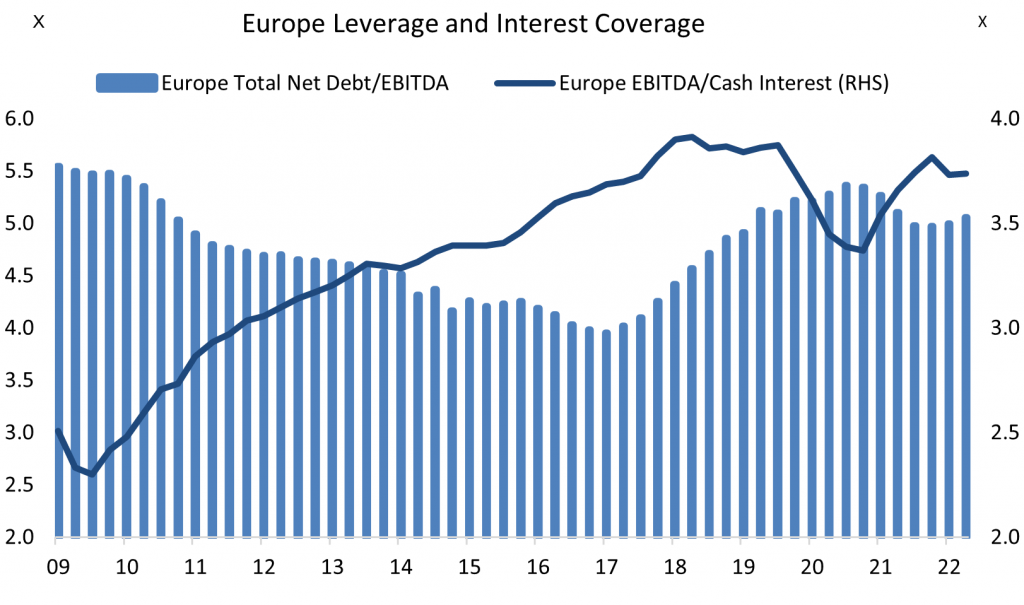

Europe’s private company balance sheets, as tracked by ICG’s private company database, also enter this more difficult period on strong foundations. At an aggregate level, strong EBITDA growth helped push leverage down and interest coverage up through to the end of 2021, with both stabilising at healthy levels in the first half of 2022.

The trend towards improved credit fundamentals through 2021 and in 2022 is corroborated by credit rating agency data. According to S&P, Europe’s speculative-grade corporate default rate was 1.7% at end of June 2022, down from a peak of 5.5% in November 2020 and 1.9% in January 2020 before the pandemic hit.

Strong private company balance sheets

Bank balance sheets substantially sounder than 2008/09

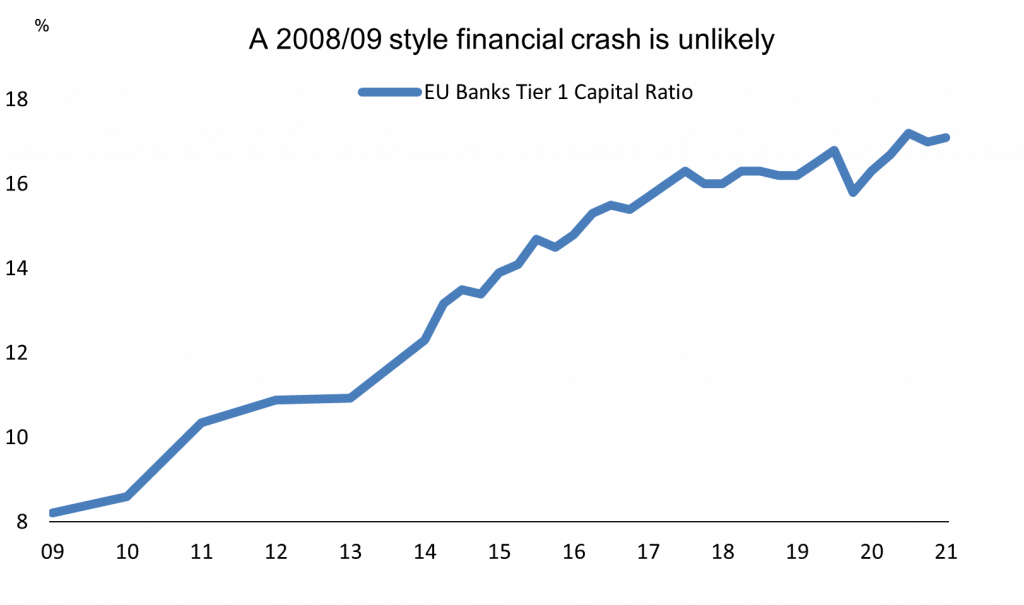

Bank balance sheets are also strong. While banks are likely to become more conservative in credit provision, Europe and UK banks tier one capital is more than double 2008 levels and regular stress indicates they are well-buffered against weaker growth. In addition, while the ECB is expected to continue to raise rates in the coming months, it has also made clear that through its new Transmission Protection Instrument (TPI), PEPP reinvestments, OMT and other market intervention mechanisms that it has the tools, and has the will, to do “whatever it takes” to protect against sovereign bond market stress (with Italy clearly front of mind). These factors make a repeat of a 2008/09 or Euro style systemic financial crisis unlikely in our view.

European Banks are well-capitalised

Inflation poised to fall in 2023

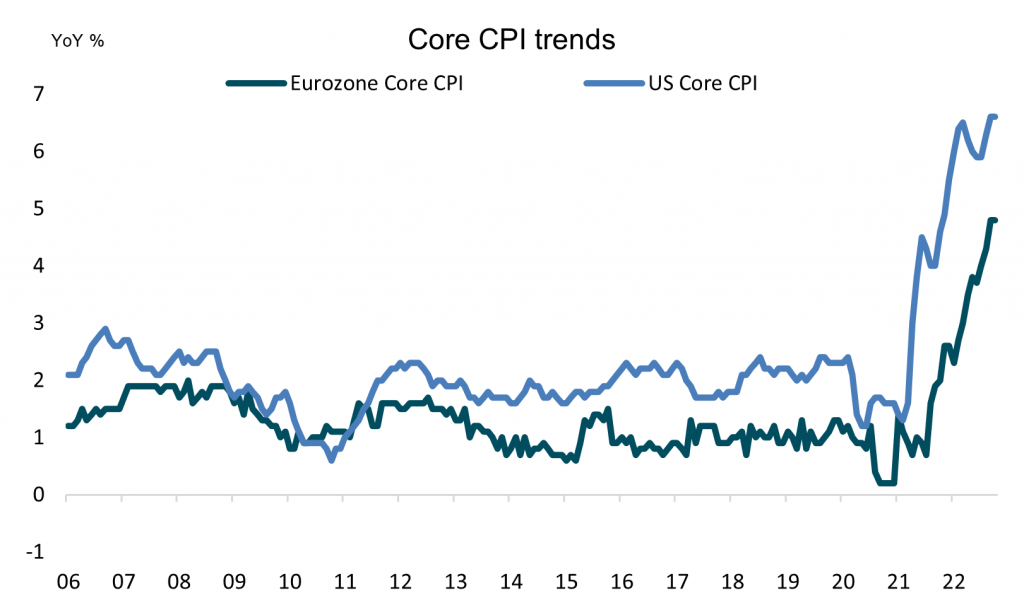

Assuming energy prices remain below 2022 highs, inflation should fall quickly in the latter part of 2023 – particularly in Europe – taking pressure off interest rates and reducing the squeeze on disposable incomes as the impact of higher energy prices rolls out of inflation calculations and core inflation eases. Core (non-food and energy) inflation has been less pronounced in Europe than in the US, with the rise in energy and food prices contributing to nearly 50% of the increase in Eurozone headline inflation.

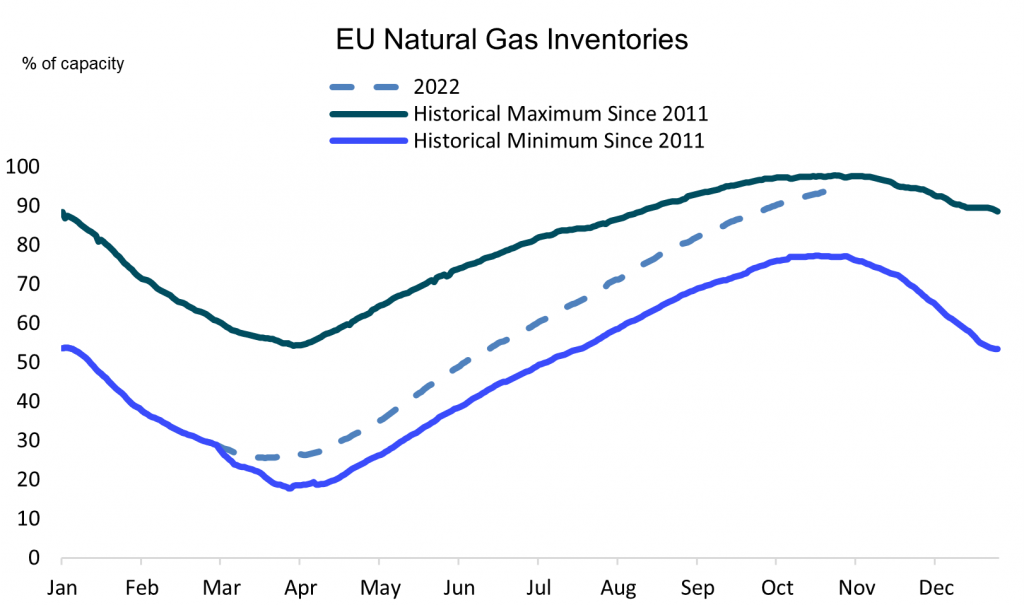

If energy and food prices remain flat or fall in 2023 (Europe’s benchmark front month natural gas price is now down around 70% from its August peak and EU natural gas storage in October was 94%, near an all-time high), the base effect alone should drive headline inflation sharply lower. Input costs will also likely moderate as supply chain bottlenecks and labour markets ease and property markets cool. This should allow Euro rates to remain significantly below US rates and alleviate downward pressure on domestic demand in 2023 in our view.

Eurozone inflation more muted than US

EU natural gas supplies near record level

Substantial fiscal support

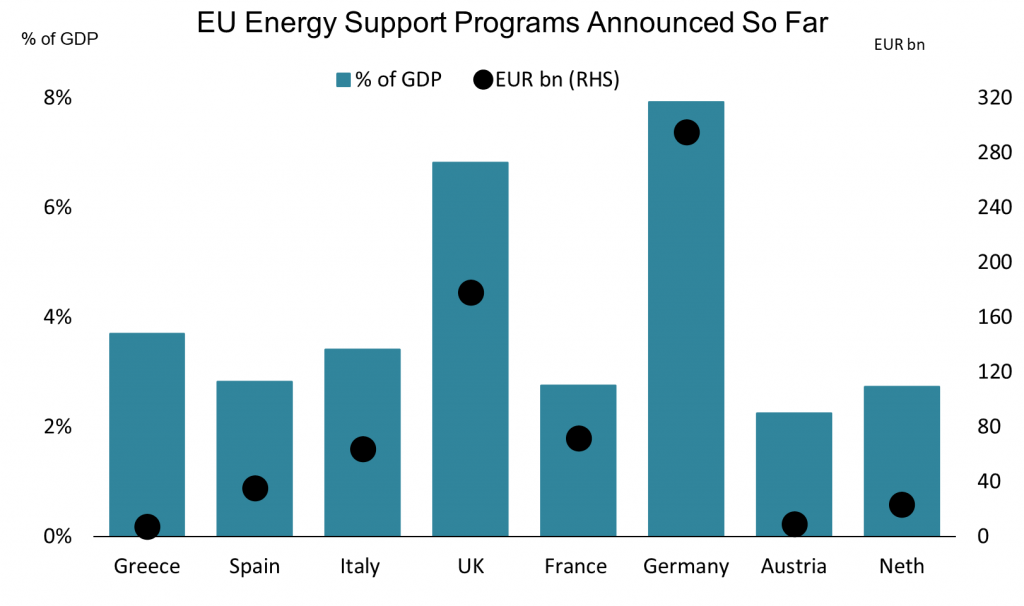

And last, but certainly not least, governments are putting together substantial fiscal packages to support businesses and households hit by the rise in energy prices. Already the UK and a number of governments in Europe have acted to shield households from higher energy costs through varying combinations of energy tax cuts, subsidies, direct payments and price caps. Support for households and businesses announced by the UK is estimated to potentially be equivalent to close to 8% of GDP. Germany recently announced a €200bn package and other government across Europe are acting swiftly to provide support. In addition, there are also still substantial funds from the EU’s €800 Next Generation EU recovery programme to be disbursed. More announcements on fiscal support packages to protect economies from the energy and food price shock are likely in the coming months.

If effectively implemented, the support programs should go a long way to protecting households and companies from the worst of the energy price squeeze.

Large-scale fiscal support on the way

Europe is not homogeneous: Country performance to diverge

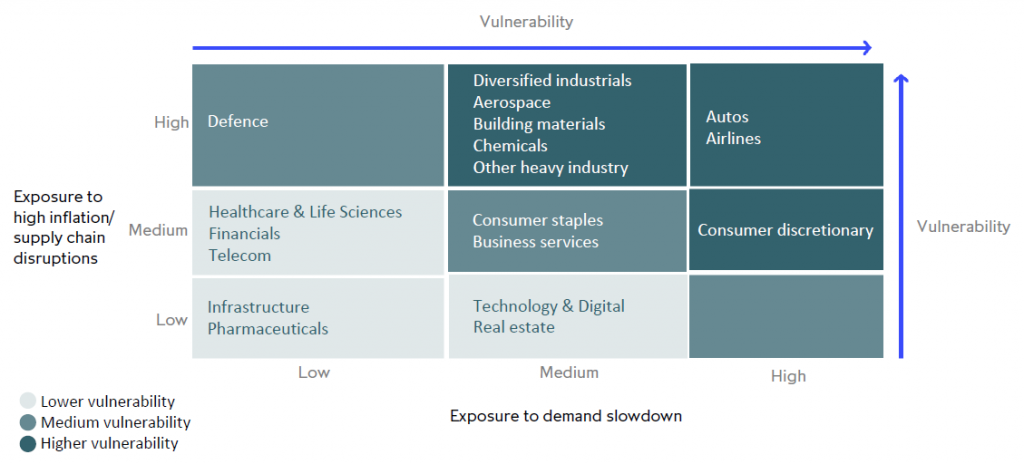

Country performance is also likely to diverge, and even within countries, sector performance variation is likely to be high. While Germany and Italy’s large exposures to energy intensive industry and auto production are likely to cause their headline GDP growth rates to slow quite sharply over the next few quarters, less fossil fuel dependent countries in the Nordics are likely to see limited impact. France, Spain and Portugal will also likely be less affected with more diverse energy sources and a higher proportion of tourism and other services. Across all countries the impact is likely to focused mostly in the industrial and consumer discretionary sectors.

As during the Covid-19 pandemic, differentiation at a sector level will be a critical factor driving investment performance over the coming quarters, not headline GDP growth rates.

In the UK, the new Rishi Sunak led government has restored confidence following the market turmoil caused by the (very short-lived) Truss government, with bond yields and the pound back to pre “mini-budget” levels. The UK consumer is likely to suffer over the next few quarters as higher energy prices and interest rates eat into disposable income, with negative implications for the consumer discretionary sector. However, highly internationally competitive sectors such as healthcare and biotech, technology and business services, as well as consumer staples should see much more limited impact.

Country growth will vary widely

Not all sectors are created equal

The slowdown in growth is likely to be highly sector specific, with less affected sectors continuing to outperform despite a broader economic slowdown. Less cyclical and less energy-intensive sectors such as healthcare and biotech, technology and software, business and financial services are likely to hold up relatively well over the next quarters in our view.

Energy price-sensitive sectors such as chemicals and heavy industry, aviation, autos, building materials and big-ticket consumer discretionary will likely take the brunt of the hit. And some sectors, such as green infrastructure, sustainable transport, businesses supporting green transition, LNG and pipeline services will likely see a sustained structural boost to demand.

As during the Covid-19 pandemic, differentiation at a sector level will be a critical factor driving investment performance over the coming quarters, not headline GDP growth rates. This likely was a key factor allowing private companies as tracked by ICG’s private company database perform so strongly through the pandemic period despite the sharp fall in headline economic growth.

Disruption brings opportunity

Market disruption and wide performance dispersion at a country, sector and sub sector level brings opportunity for investors with medium to long-term investment horizons, strong bottom-up analytical skills, local knowledge, flexible capital and close working relationships with investee companies. With public market volatility likely to remain high and banks continuing to retrench, this environment should be particularly suited to private market investors in our view.

Sector performance will vary widely